Hi,

My 401k makes it hard for me to do a pure PP. I'm thinking about doing a VP to use some of the low expense ratio 401k offerings and maybe complement my PP. One fund I'm thinking of for the VP is the PIMCO Total Return Fund, which we get with a 0.46% exp ratio, which I understand is fairly low for this popular fund. We also have an international equity index fund available with a 0.15% exp ratio.

For my VP, I'm thinking of 50% in the PIMCO fund and 50% in the international equity index fund. The only other idea I have is 50% in the PIMCO and 50% in the S&P500 index fund (0.05% ER), but I've already got that last one in my PP.

The only other available funds with fairly low exp ratios are a large cap growth fund at 0.54% ER, a large-cap income fund with 0.4% ER, a total U.S. corporate/gov bond index with 0.13 % ER, and a Wellington TIPS with a 0.175% ER.

Does anyone have any advice for me? Again, I'm trying to complement my PP as much as possible for additional diversification, and maybe a little higher risk/reward, since I'm only in my 40s. If I could just do a pure PP, I'd probably do that, but my 401k makes that impossible.

Thanks.

VP Input Request

Moderator: Global Moderator

-

Pointedstick

- Executive Member

- Posts: 8886

- Joined: Tue Apr 17, 2012 9:21 pm

- Contact:

Re: VP Input Request

You could do a Boglehead 60/40 portfolio with the S&P500 index and total bond fund, watering it down with some amount of the total return fund to suit your risk tolerance. Not ideal compared to a PP of course, but serviceable.

Human behavior is economic behavior. The particulars may vary, but competition for limited resources remains a constant.

- CEO Nwabudike Morgan

- CEO Nwabudike Morgan

-

Ad Orientem

- Executive Member

- Posts: 3483

- Joined: Sun Aug 14, 2011 2:47 pm

- Location: Florida USA

- Contact:

Re: VP Input Request

Unless you are wealthy, or at least financially independent to the point where you can take a big hit and not lose sleep, I would invest 401k money conservatively. A PP is ideal but for many people it's just not practical. In that case you go with plan B. Plan B for conservative investments will vary depending on your available options. But the basic rules still apply...

1. Index. There is a mountain of evidence that has established, IMHO beyond the point where it's debatable, that actively managed portfolios will underperform passively managed portfolios over the long run unless your swinging for the fences with highly concentrated high risk speculations. Then you MIGHT beat the index, but the odds are heavily stacked against you.

2. Your unlikely to go too far wrong with a Jack Bogle type portfolio. Think either 50/50 bonds and stocks with a 60/40 rebalancing band or the old rule of 1% bonds for each year of your age up to around 75. If you are sticking with a straight stock bond portfolio you will want to add some currency diversification. I suggest using a low cost cap weighted global stock market index/ETF fund like VT. It is not as good as gold but it's better than being all in the dollar.

3. Another good choice if available might be VWINX (I am presuming that PRPFX is not an option).

Edit: Typo

1. Index. There is a mountain of evidence that has established, IMHO beyond the point where it's debatable, that actively managed portfolios will underperform passively managed portfolios over the long run unless your swinging for the fences with highly concentrated high risk speculations. Then you MIGHT beat the index, but the odds are heavily stacked against you.

2. Your unlikely to go too far wrong with a Jack Bogle type portfolio. Think either 50/50 bonds and stocks with a 60/40 rebalancing band or the old rule of 1% bonds for each year of your age up to around 75. If you are sticking with a straight stock bond portfolio you will want to add some currency diversification. I suggest using a low cost cap weighted global stock market index/ETF fund like VT. It is not as good as gold but it's better than being all in the dollar.

3. Another good choice if available might be VWINX (I am presuming that PRPFX is not an option).

Edit: Typo

Last edited by Ad Orientem on Sun Apr 07, 2013 12:35 pm, edited 1 time in total.

Trumpism is not a philosophy or a movement. It's a cult.

Re: VP Input Request

You actually could replicate a PP pretty easily with those offerings.

20% Stocks

60% TBM

20% gold

is actually pretty close to the PP. The TBM is very roughly similar to a the cash/LTT barbell, but slightly less volatile so you have to bump the weightings.

The gold could just be physical bullion which unfortunately would be in taxable, but the PP is not impossible to achieve. At the end of the day the PP is not too far from a bond heavy boglehead portfolio with a slug of gold thrown in.

Now if you want something different from the PP that is fine too, but those offerings don't prevent you from constructing something very similar.

20% Stocks

60% TBM

20% gold

is actually pretty close to the PP. The TBM is very roughly similar to a the cash/LTT barbell, but slightly less volatile so you have to bump the weightings.

The gold could just be physical bullion which unfortunately would be in taxable, but the PP is not impossible to achieve. At the end of the day the PP is not too far from a bond heavy boglehead portfolio with a slug of gold thrown in.

Now if you want something different from the PP that is fine too, but those offerings don't prevent you from constructing something very similar.

everything comes from somewhere and everything goes somewhere

-

Ad Orientem

- Executive Member

- Posts: 3483

- Joined: Sun Aug 14, 2011 2:47 pm

- Location: Florida USA

- Contact:

Re: VP Input Request

In light of melveyr's post I would add that my own recommendations were made under the impression that gold is not an available option in your 401k. If it is, you should definitely have some (at least 10%).

Trumpism is not a philosophy or a movement. It's a cult.

Re: VP Input Request

Stuper1 - Does the 401k plan have a brokerage window? - If so you can purchase the gold in the form of an ETF (IAU) via the brokerage service. Something to check into..

Re: VP Input Request

Thanks to all for the input so far. Just to clarify what melveyr and desert are saying, when you recommend TBM, you are talking about the total U.S. corp/gov bond index fund and not the PIMCO Total Return fund. Is that correct?

Re: VP Input Request

Yes, that's the index it uses. This TBM fund has an average maturity of 6.34 years. If I use 25 years as the average maturity for LTT bonds and 0.5 year as the avg mat for cash, then my calculation tells me that this TBM index fund should be considered as about 24% LTT bonds and 76% cash. Here's the calculation:

(24% * 25 yrs + 76% * 0.5 yrs) / 100% = 6.38 year

Am I looking at this the right way? Should I really consider this TBM index as 24% bonds and 76% cash? It will work if that's the right thing to do, because I have some Roth IRA money that I can use to buy more bonds. I just want to make sure I'm doing this the right way.

And yes, to answer another question, I do have a brokerage window in the 401k to buy gold, as well as the Roth IRA option to buy gold. So I do have some options, and thank you for the advice.

(24% * 25 yrs + 76% * 0.5 yrs) / 100% = 6.38 year

Am I looking at this the right way? Should I really consider this TBM index as 24% bonds and 76% cash? It will work if that's the right thing to do, because I have some Roth IRA money that I can use to buy more bonds. I just want to make sure I'm doing this the right way.

And yes, to answer another question, I do have a brokerage window in the 401k to buy gold, as well as the Roth IRA option to buy gold. So I do have some options, and thank you for the advice.

-

Ad Orientem

- Executive Member

- Posts: 3483

- Joined: Sun Aug 14, 2011 2:47 pm

- Location: Florida USA

- Contact:

Re: VP Input Request

If you have the option of buying gold but are unable to construct a PP for some other reason I would go with 50% TBM 30% Global Stock Market Index or if that's not an option then TSM and 20% gold. If you are using a gold ETF then IAU is probably your best bet.

Trumpism is not a philosophy or a movement. It's a cult.

-

Pointedstick

- Executive Member

- Posts: 8886

- Joined: Tue Apr 17, 2012 9:21 pm

- Contact:

Re: VP Input Request

Oh, well that changes everything! You can probably make a whole PP in your 401k:stuper1 wrote: And yes, to answer another question, I do have a brokerage window in the 401k to buy gold, as well as the Roth IRA option to buy gold. So I do have some options, and thank you for the advice.

- 25% S&P500 fund in the regular part of your 401k, with the remaining 75% put in the brokerage part and invested in:

-- 25% individual 30-year treasuries

-- 25% individual T-bills

-- 25% IAU (lowest ER of the ETFs)

This is what I do in my 401k since I'm lucky to have a brokerage window and the option to invest up to 95% of my funds in the brokerage portion.

Some of the details depend on the brokerage, e.g. if it's with Schwab, you can get SGOL commission-free, if it's with Fidelity or TDAmeritrade you can have them make you an easy T-bill ladder, and so on and so forth.

Human behavior is economic behavior. The particulars may vary, but competition for limited resources remains a constant.

- CEO Nwabudike Morgan

- CEO Nwabudike Morgan

Re: VP Input Request

I can only put up to 25% of my 401k money in the brokerage window, which makes things a little difficult. The bottom line is that I have to buy some of the TBM index in the 401k. My main remaining question is whether to consider that TBM money as 50% bonds and 50% cash, or 24% bonds and 76% cash (as shown in my previous post), or some other split. Any input on this will be greatly appreciated. Thanks!

-

Ad Orientem

- Executive Member

- Posts: 3483

- Joined: Sun Aug 14, 2011 2:47 pm

- Location: Florida USA

- Contact:

Re: VP Input Request

I wouldn't obsess over that breakdown as you are not creating a PP. Just figure 50% TBM 30% stocks (global index if available otherwise S&P 500 or TSM is fine) and 20% in gold. That should give you a pretty robust portfolio that will hold up in most situations and provide you with a decent return over the long run.stuper1 wrote: I can only put up to 25% of my 401k money in the brokerage window, which makes things a little difficult. The bottom line is that I have to buy some of the TBM index in the 401k. My main remaining question is whether to consider that TBM money as 50% bonds and 50% cash, or 24% bonds and 76% cash (as shown in my previous post), or some other split. Any input on this will be greatly appreciated. Thanks!

Trumpism is not a philosophy or a movement. It's a cult.

-

Pointedstick

- Executive Member

- Posts: 8886

- Joined: Tue Apr 17, 2012 9:21 pm

- Contact:

Re: VP Input Request

Absolutely. I would be totally happy with such a portfolio if I had one myself, personally. Any "bond heavy boglehead portfolio with a slug of gold thrown in" (love that wording!) as melveyr described will be very robust. It doesn't have to be perfect to be faithful to the PP idea, and that's not a bad compromise at all when you're talking about restrictive 401ks.Ad Orientem wrote: I wouldn't obsess over that breakdown as you are not creating a PP. Just figure 50% TBM 30% stocks (global index if available otherwise S&P 500 or TSM is fine) and 20% in gold. That should give you a pretty robust portfolio that will hold up in most situations and provide you with a decent return over the long run.

[align=center]

[/align]

[/align]Human behavior is economic behavior. The particulars may vary, but competition for limited resources remains a constant.

- CEO Nwabudike Morgan

- CEO Nwabudike Morgan

Re: VP Input Request

stuper1,

By not going with a 4x25 you have opened Pandora's box. Since it is open, let's make the most of it and try build you a robust portfolio that is inspired by the PP's principles.

The PP is designed to roughly allocate risk between stocks, LTT, and gold. These three volatile components are the most important part of the portfolio. The cash component largely waters down the portfolio; it is not the whiskey! Some people like their drink to be strong (0% cash and 33% in the other assets) or another might prefer it to be weak (70% in cash and 10% in the other components). I wouldn't obsess over trying to perfectly match HB's 25% cash prescription because there is nothing fundamental about it, it was just due to the nice aesthetics of a 4x25 split.

So, it appears that your 401k has gold (through the window), stocks, and TBM. A Permanent Portfolio of these assets would be the portfolio that equally allocated risk across these asset classes. Using simba's spreadsheet and some math ( http://www.thierry-roncalli.com/download/erc-slides.pdf ), I have calculate that a portfolio of 62.5% TBM, 20% stocks, and 17.5% gold has historically been the portfolio that equally allocated risk amongst these three assets. It is balanced. It is less volatile than the PP so I don't think cash would be necessary unless the normal PP was too volatile as well.

In my earlier post I rounded everything to 60/20/20 (bonds/stocks/gold), but I thought it would be worth going into detail how I came up with it. Also, the 62.5/20/17.5 portfolio has 0.93 correlation with the PP. It is basically just as good (or possibly better )

)

By not going with a 4x25 you have opened Pandora's box. Since it is open, let's make the most of it and try build you a robust portfolio that is inspired by the PP's principles.

The PP is designed to roughly allocate risk between stocks, LTT, and gold. These three volatile components are the most important part of the portfolio. The cash component largely waters down the portfolio; it is not the whiskey! Some people like their drink to be strong (0% cash and 33% in the other assets) or another might prefer it to be weak (70% in cash and 10% in the other components). I wouldn't obsess over trying to perfectly match HB's 25% cash prescription because there is nothing fundamental about it, it was just due to the nice aesthetics of a 4x25 split.

So, it appears that your 401k has gold (through the window), stocks, and TBM. A Permanent Portfolio of these assets would be the portfolio that equally allocated risk across these asset classes. Using simba's spreadsheet and some math ( http://www.thierry-roncalli.com/download/erc-slides.pdf ), I have calculate that a portfolio of 62.5% TBM, 20% stocks, and 17.5% gold has historically been the portfolio that equally allocated risk amongst these three assets. It is balanced. It is less volatile than the PP so I don't think cash would be necessary unless the normal PP was too volatile as well.

In my earlier post I rounded everything to 60/20/20 (bonds/stocks/gold), but I thought it would be worth going into detail how I came up with it. Also, the 62.5/20/17.5 portfolio has 0.93 correlation with the PP. It is basically just as good (or possibly better

Last edited by melveyr on Mon Apr 08, 2013 12:00 am, edited 1 time in total.

everything comes from somewhere and everything goes somewhere

-

Ad Orientem

- Executive Member

- Posts: 3483

- Joined: Sun Aug 14, 2011 2:47 pm

- Location: Florida USA

- Contact:

Re: VP Input Request

melveyr

It seems to me that your proposal is based on the available data going back forty years or so. But that can be misleading. In that time frame we have experienced neither an exceptionally severe deflation nor a severe inflation (the 1970's while unpleasant could hardly be classified as severe inflation). The PP is designed to offer downside protection and at least the hope of profit in any of the four generally accepted economic conditions.

I would certainly love to be 60%+ in bonds with only a 20% allocation in stocks if we had a nasty deflationary crisis or even another 2008-09. But by under-weighting equities and gold it seems that your portfolio might lag during periods of strong economic expansion and prosperity. And in the event of a sharp rise in interest rates and or inflation it could take a nasty hit.

Conversely my own suggestion of 50-30-20 has its drawbacks too. The bond allocation might be a bit low for a severe deflation (think 1930's). But I doubt it would take a crushing hit especially if you are not entirely in domestic stocks (one of the lessons of the great Japanese deflation).

Of course once you move out of the PP optimum asset allocation is not so clearly laid out. But at the risk of sounding like a stock bug (which I am not) I do take note that historically stocks have tended to outperform bonds over the long run. If I had to hedge a portfolio in one direction or another, and presuming I had a long ways (20 or so years) to retirement, I think I would give that little bit of extra weight to stocks over bonds. If I were closer to retirement I might lean a bit more towards your more bond heavy allocation.

But yeah, with bonds yields at or near record lows, likewise official CPI, underweighting equities and gold so dramatically in favor of bonds would require a level of nerve that I am not sure I posses.

It seems to me that your proposal is based on the available data going back forty years or so. But that can be misleading. In that time frame we have experienced neither an exceptionally severe deflation nor a severe inflation (the 1970's while unpleasant could hardly be classified as severe inflation). The PP is designed to offer downside protection and at least the hope of profit in any of the four generally accepted economic conditions.

I would certainly love to be 60%+ in bonds with only a 20% allocation in stocks if we had a nasty deflationary crisis or even another 2008-09. But by under-weighting equities and gold it seems that your portfolio might lag during periods of strong economic expansion and prosperity. And in the event of a sharp rise in interest rates and or inflation it could take a nasty hit.

Conversely my own suggestion of 50-30-20 has its drawbacks too. The bond allocation might be a bit low for a severe deflation (think 1930's). But I doubt it would take a crushing hit especially if you are not entirely in domestic stocks (one of the lessons of the great Japanese deflation).

Of course once you move out of the PP optimum asset allocation is not so clearly laid out. But at the risk of sounding like a stock bug (which I am not) I do take note that historically stocks have tended to outperform bonds over the long run. If I had to hedge a portfolio in one direction or another, and presuming I had a long ways (20 or so years) to retirement, I think I would give that little bit of extra weight to stocks over bonds. If I were closer to retirement I might lean a bit more towards your more bond heavy allocation.

But yeah, with bonds yields at or near record lows, likewise official CPI, underweighting equities and gold so dramatically in favor of bonds would require a level of nerve that I am not sure I posses.

Trumpism is not a philosophy or a movement. It's a cult.

Re: VP Input Request

That's a low ER for the PIMCO fund. I manage my wife's 401K and she has access to the D class shares of that fund, but at 0.75% ER.stuper1 wrote: My 401k makes it hard for me to do a pure PP. I'm thinking about doing a VP to use some of the low expense ratio 401k offerings and maybe complement my PP. One fund I'm thinking of for the VP is the PIMCO Total Return Fund, which we get with a 0.46% exp ratio, which I understand is fairly low for this popular fund.

The whole aim of practical politics is to keep the populace alarmed (and hence clamorous to be led to safety) by menacing it with an endless series of hobgoblins, all of them imaginary.

- H. L. Mencken

- H. L. Mencken

Re: VP Input Request

Ad,Ad Orientem wrote: melveyr

It seems to me that your proposal is based on the available data going back forty years or so. But that can be misleading. In that time frame we have experienced neither an exceptionally severe deflation nor a severe inflation (the 1970's while unpleasant could hardly be classified as severe inflation). The PP is designed to offer downside protection and at least the hope of profit in any of the four generally accepted economic conditions.

I would certainly love to be 60%+ in bonds with only a 20% allocation in stocks if we had a nasty deflationary crisis or even another 2008-09. But by under-weighting equities and gold it seems that your portfolio might lag during periods of strong economic expansion and prosperity. And in the event of a sharp rise in interest rates and or inflation it could take a nasty hit.

The allocation that I proposed had an equal risk allocation between stocks, gold, and bonds from 1972-2011. Although the dollar amounts make it look bond heavy, the portfolio performance was equally explained by the three asset classes. The risk allocation was 33.3%, 33.3% and 33.3%.

You are totally right that we have no idea if an allocation will continue to be balanced in the future as it was in the past, but we can say the same for the PP.

To better explain the concept, a portfolio of 60/40 stocks/TBM has a risk allocation of 90/10. Where as a portfolio of 60/40 stocks/LTT has a risk allocation of 80/20. Different bonds contribute different amounts to the risk budget, and TBM has a much weaker contribution than LTT so you have to hold more of it to achieve risk parity.

With the portfolio I proposed you would not be "rooting" for bonds when you fell asleep. You would be ambivalent between the asset classes because each would play an equal role in portfolio performance.

Last edited by melveyr on Mon Apr 08, 2013 10:26 am, edited 1 time in total.

everything comes from somewhere and everything goes somewhere

Re: VP Input Request

As per usual, melveyr, you're a gold mine of information (pun intended). That is a very practical plan for the 401K shenanigans we've all struggled with.

I have a similar problem in my TIAA-CREF account, which I need to keep separate from the PP for multiple reasons - not the least of which that I'm planning to take the annuity option at age 65. I went with the standard 60/40 portfolio, with 20% real estate included in the stock piece. There's no gold option of course.

One moderately strange choice I made was to split the bond portion between total bond, TIPS, and TIAA traditional (a stable value fund). In my opinion total bond is a great asset but it correlates too closely with stocks to be a good diversifier. I dislike TIPS because they are probably useless in a serious deflation, but it's the only fund in the plan that is predominantly treasuries. What do you think of this? Stuper1, do you have a TIPS fund in your plan?

I have a similar problem in my TIAA-CREF account, which I need to keep separate from the PP for multiple reasons - not the least of which that I'm planning to take the annuity option at age 65. I went with the standard 60/40 portfolio, with 20% real estate included in the stock piece. There's no gold option of course.

One moderately strange choice I made was to split the bond portion between total bond, TIPS, and TIAA traditional (a stable value fund). In my opinion total bond is a great asset but it correlates too closely with stocks to be a good diversifier. I dislike TIPS because they are probably useless in a serious deflation, but it's the only fund in the plan that is predominantly treasuries. What do you think of this? Stuper1, do you have a TIPS fund in your plan?

"Democracy is two wolves and a lamb voting on what to have for lunch." -- Benjamin Franklin

Re: VP Input Request

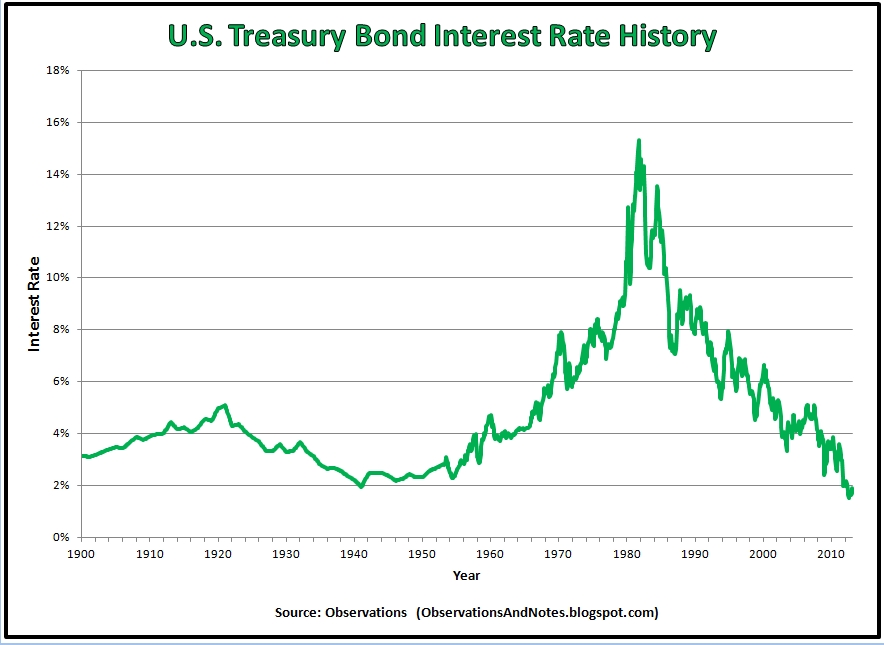

1972 may sound like a long time, but it is still biased toward declining treasury yields, isn't it? Sure would be interesting if one could know the most balanced allocation going back to 1950. Here is a plot of the 10 yr T Note:melveyr wrote: The allocation that I proposed had an equal risk allocation between stocks, gold, and bonds from 1972-2011. Although the dollar amounts make it look bond heavy, the portfolio performance was equally explained by the three asset classes. The risk allocation was 33.3%, 33.3% and 33.3%.

Re: VP Input Request

Well it would be very simple to calculate with regards to stocks and 10 year Treasuries, but unfortunately we wouldn't be able to test for gold's role in that portfolio so I think we are stuck with the data we haveBearBones wrote:1972 may sound like a long time, but it is still biased toward declining treasury yields, isn't it? Sure would be interesting if one could know the most balanced allocation going back to 1950. Here is a plot of the 10 yr T Note:melveyr wrote: The allocation that I proposed had an equal risk allocation between stocks, gold, and bonds from 1972-2011. Although the dollar amounts make it look bond heavy, the portfolio performance was equally explained by the three asset classes. The risk allocation was 33.3%, 33.3% and 33.3%.

Additionally your critique would be just as valid for the PP as the alternate portfolio that I proposed. We shouldn't operate under the assumption that PP is some holy grail that is perfectly balanced just because it has equal dollar weightings. Dollar weightings don't drive portfolio performance, but risk weightings do. Besides even if the PP was some holy grail the portfolio I proposed has 0.93 correlation to it.

Last edited by melveyr on Mon Apr 08, 2013 2:24 pm, edited 1 time in total.

everything comes from somewhere and everything goes somewhere

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: VP Input Request

As I've learned more about the different portfolio weighting schemes, I take umbrage at your use of the word "roughly". I would say sloppily instead. All the PP's equal weight scheme does is avoid concentration risk. Nothing more, nothing less. Since that is all it does, it ranks dead last on a risk-reward basis compared to other schemes. Now, granted, the PP has low transanction costs which sink many of the other schemes that rely on too frequent rebalancings for outperformance and it is also a simple heuristic strategy, not requiring a complex and computationally-intensive algorithm mandating a ENIAC mainframe to operate. The eggheads can go too far...melveyr wrote: The PP is designed to roughly allocate risk between stocks, LTT, and gold. These three volatile components are the most important part of the portfolio. The cash component largely waters down the portfolio; it is not the whiskey! Some people like their drink to be strong (0% cash and 33% in the other assets) or another might prefer it to be weak (70% in cash and 10% in the other components). I wouldn't obsess over trying to perfectly match HB's 25% cash prescription because there is nothing fundamental about it, it was just due to the nice aesthetics of a 4x25 split

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: VP Input Request

The problem with minimum variance (the lowest portfolio on the Efficient Frontier), volatility weighting (risk parity) or equal risk contribution weighting schemes is that they overweight to the lowest volatility asset and we don't have enough historical data to capture the trough to trough bear market in T-Bonds starting around 1940. So they will naturally overweight it. There are a number of ways around this but none which are particularly muppet friendly or empirically pleasing.BearBones wrote: 1972 may sound like a long time, but it is still biased toward declining treasury yields, isn't it? Sure would be interesting if one could know the most balanced allocation going back to 1950. Here is a plot

We all tend to overlook that the PP is a fundamental approach at heart and get caught up in the technical portfolio minutia because that is most easily amenable to quantification.

Last edited by MachineGhost on Mon Apr 08, 2013 6:00 pm, edited 1 time in total.

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Re: VP Input Request

Lost me there. Can you explain?MachineGhost wrote: We all tend to overlook that the PP is a fundamental approach at heart and get caught up in the technical portfolio minutia because that is most easily amenable to quantification.

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: VP Input Request

From what I've seen, it is far too easy to measure the covariance or correlation of assets over a limited period of history that won't capture all possible permutations. The PP is derived from a fundamental theory, not a result of mathematical optimization. (And if we believe the claim that Browne & Coxon used a old-school supercomputer to derive the PRPFX portfolio from a century of market data, what exactly did they do about the gold standard pre-1971?)BearBones wrote: Lost me there. Can you explain?

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Re: VP Input Request

MG,MachineGhost wrote:From what I've seen, it is far too easy to measure the covariance or correlation of assets over a limited period of history that won't capture all possible permutations. The PP is derived from a fundamental theory, not a result of mathematical optimization. (And if we believe the claim that Browne & Coxon used a old-school supercomputer to derive the PRPFX portfolio from a century of market data, what exactly did they do about the gold standard pre-1971?)BearBones wrote: Lost me there. Can you explain?

I am still not quite sure where you stand. You criticize the PP and call its followers muppets in one breath (alluding to a better quantitative solution that involves more transactions), but then you dismiss quantitative solutions in posts like this.

Where do you stand? What are you currently doing with your money?

everything comes from somewhere and everything goes somewhere