Interesting editorial in today's WSJ. Guess I will be changing Schwab ETFs for Vanguard's.

- Screenshot 2023-05-16 140051.png (34.41 KiB) Viewed 29372 times

wsj.com

Opinion | The ESG Proxy Vote Ranking

The Editorial Board

4–5 minutes

Is your asset manager voting based on the interests of investors or for political agendas?

May 15, 2023 6:21 pm ET

If Americans want to make investment decisions using environmental, social and governance factors, that’s fair enough. It’s a free country. The problem is having a hidden agenda that applies to everybody else. A new analysis says that, even in non-ESG investment vehicles, many asset managers proxy vote in favor of woke shareholder proposals to do racial audits or strangle fossil fuels.

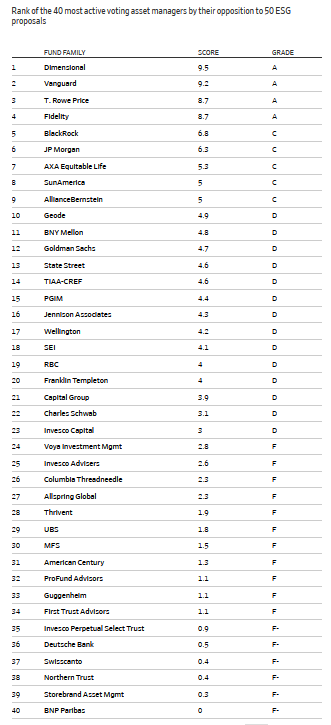

The table nearby shows the score. It’s from a report by the Committee to Unleash Prosperity, which examined “4,814 non-ESG branded funds” to see how proxy votes were cast on “50 of the most extreme ESG-oriented shareholder proposals from 2022.” One proposal wanted Home Depot to perform a “racial equity audit” to identify “adverse impacts on nonwhite stakeholders.” Another called on Costco to set climate targets for “Scope 3” emissions, including due to “land use change” and “deforestation.” Neither has anything to do with the bottom line.

Among the top 40 most active voters, the report gives an A grade to Dimensional, Vanguard, T. Rowe Price, and Fidelity, a signal that they respect savers and investors who have differing views on today’s heated political debates. “We don’t believe that we should dictate company strategy,” Vanguard CEO Tim Buckley recently said regarding climate change. “It would be hubris to presume that we know the right strategy for the thousands of companies that Vanguard invests with.”

The report awards an F-minus to six top-40 firms that backed more than 90% of the ESG proposals. Drum roll, please: Invesco Perpetual Select Trust, Deutsche Bank, Swisscanto, Northern Trust, Storebrand Asset Management, and BNP Paribas. Other prominent firms that received a D or an F grade include Goldman Sachs, State Street, TIAA-CREF, Charles Schwab, UBS, and Guggenheim.

How about Larry Fink’s BlackRock? It gets a C grade. The report says BlackRock “has begun to retreat from its ESG advocacy on proxy voting as shareholder proposals have become more extreme.” Also quoted is a BlackRock statement last year that “many of the climate-related shareholder proposals coming to a vote in 2022 are more prescriptive or constraining on companies and may not promote long-term shareholder value.” Mugged by reality?

Another surprise, or maybe not, is that ESG labeling isn’t always a reliable guide. The study says it also examined 382 funds with explicit ESG branding and found they were only “modestly more likely” to vote for these proposals. Among the fund families analyzed, 109 offered ESG and non-ESG options, yet sometimes the difference hardly mattered. “Only 58 of these met the ‘sniff test’ of voting patterns consistent with investor intent,” the report says. “Investors needs to be vigilant about where they allocate their capital, as even non-ESG funds can have a decidedly pro-ESG orientation.”

The report also calculates an imputed grade for the big two proxy advisers. Given their recommendations, Glass Lewis gets a D. ISS gets an F-minus. As shareholder proposals get wackier, perhaps they will adjust their tack, especially now that they’re getting political attention. In January a group of Republican state Attorneys General argued in a letter to Glass Lewis and ISS that they seem to have “acted contrary to the financial interests of their clients.”

Sunshine is what this ESG business demands. Pensioners and investors want a good return. What they don’t want, to pick one example, is for companies that sell paint or hamburgers to undertake costly external audits so that they can self-flagellate about the ills of the world. The Committee to Unleash Prosperity won’t have the last word, but its ranking is a good resource if you’re wondering what your asset manager is doing when you aren’t paying attention.