If they are effectively the same, why would I pick one bond over the other one? Here is an example of 30 year bonds?

Adding an example of bonds on the secondary market:

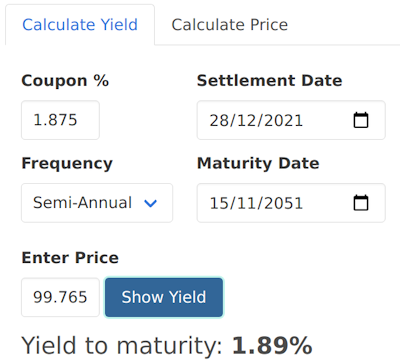

The effective yield is 1.909 vs 1.903 but the price differential is 102.484 vs 99.766. I did the math and the 102.484 (slightly different math because the price change after I did the math and before I got the screen shot so the numbers may be slightly off).

The more expensive bond came out to paying about 90ish dollars more over thirty years. Seems the same(ish). So....back to the original question.

Do I just scroll to the bottom of the offering page, grab the one with the longest duration or do I stare and compare at the offerings of the particular year LTT I want to buy?

- LTT_BOND_QUESTION.png (89.17 KiB) Viewed 5412 times