perfect_simulation wrote: ↑Sat Aug 22, 2020 12:25 am

garya505 wrote: ↑Fri Aug 21, 2020 10:09 pm

I'm curious, what was your reasoning for using the 8 largest companies instead of SPY or VTI?

The short answer is better returns. I did quite a bit of backtesting on portfoliovisualizer.com. I think the strategy is a bit aggressive, but I want that if I'm only having 25% allocated to stocks. I think a growth ETF like VUG would be a good choice too, but top8 is even beating VUG.

Perfect_simulation,

You may want to re-think this. Historically speaking, using the top eight (or top one, or top 10, or top 100) gave you

MUCH worse returns than simply using the S&P 500 as a whole. For example:

The top 1 stock vs the S&P 500: -

https://ibb.co/W3Mg2XW ; almost a ten-fold difference (in favor of the S&P 500 as a whole) vs only owning the largest (i.e. highest market cap) one stock

The top 10 largest stocks in the S&P 500 vs the S&P 500 index as a whole owned via an index fund -

https://www.bogleheads.org/forum/viewto ... 2#p5151631 ; for the last twenty years or so this gives almost a 1.5% difference per year in favor of the index as a whole.

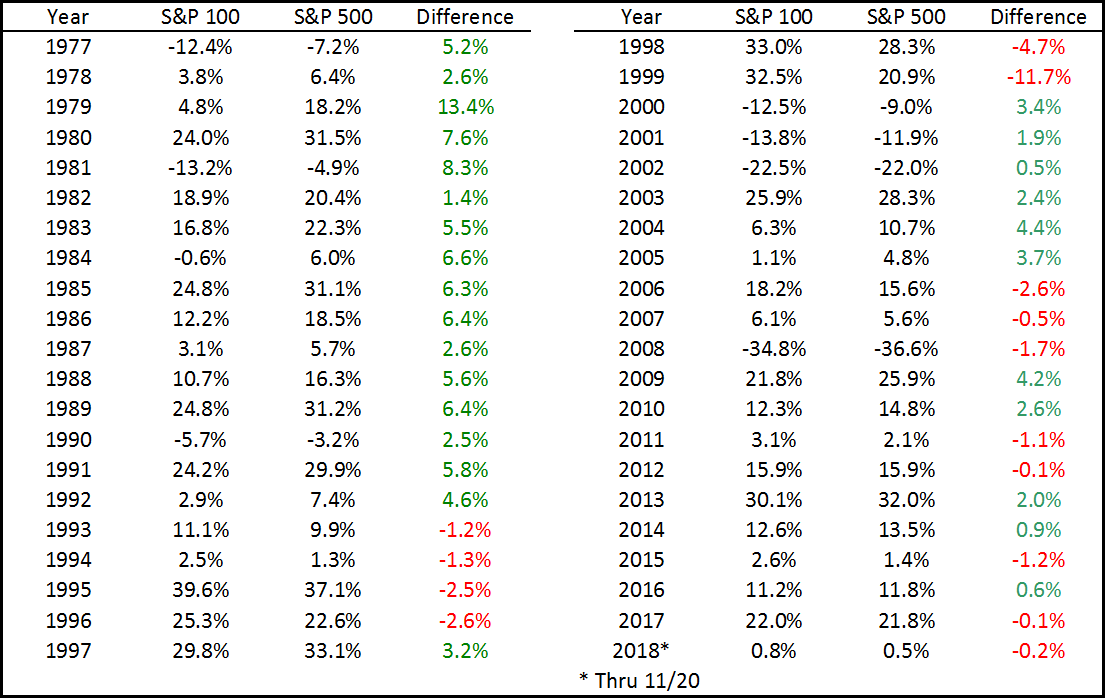

The top 100 largest stocks (AKA the S&P 100 TR Index) vs the S&P 500 TR Index -

https://webcache.googleusercontent.com/ ... clnk&gl=us ; the actual image is at

https://static.seekingalpha.com/uploads ... origin.png

In all of the above cases the S&P 500 TR outperformed the narrower slice of stock/s; the outperformance of the S&P 500 became greater as the slice became narrower and higher market cap (i.e. from S&P 100 to the top ten highest market cap stocks to the top one highest market cap stock).

FWIW I also have data for the S&P 500 Reverse Cap Weighted Index TR and the S&P 500 Equal Weight TR; going back to 1-1-1997 (which is as far back as the Reverse Cap Weighted Index goes) these indices returned a CAGR of approximately 10.31% for the Reverse Cap Weighted Index; 9.11% CAGR for the Equal Weighted Index, and only around 8.74% CAGR for the regular old market-cap weighted S&P 500 TR (and keep in mind that this is

including the most recent three years; these years--2018, 2019, and 2020 YTD--are years where the cap-weighted index has had the relatively best performance vs the other two indexes in over two decades; if you went back to December 2017 the cap-weighted index would've done even worse relative to the other two indexes). The above shows a continuation of the trend demonstrated above (i.e. the greater your weight to larger/higher market cap stocks the worse your long-term performance).

Large-cap growth stocks have really only seriously outperformed since maybe mid-2014 or early 2015. Any PV backtest that doesn't go back beyond this is a textbook example of what stock market researchers call "recency bias". With that said, perhaps this time really

IS different. Maybe the megacap MAGFANNT market darlings will continue to outperform for the next five or ten years. Who knows? The historical record is against that happening, though, and if it in fact doesn't happen, your PP variation will do much worse than a standard PP.

if you truly want to "juice" the PP's stock portion, try allocating some of it towards ETFs whose underlying factors will likely outperform over the long and very long term.....ETFs like RPV, MTUM, RSP (or RVRS), SPLV (or XRLV or USMV), or maybe a small cap value ETF/mutual fund, with perhaps a few percent (out of the 25% stock allocation total) in TQQQ or UPRO so that if the megacap high-multiple large growth stocks do well you still don't miss out on all the action but if they don't then you haven't totally screwed yourself either.

{kind=link}