Yes, likely is the level of certainty we're at. If I knew for sure that bonds would tank, I'd be scrambling to set up my own hedge fundDesert wrote:That's a very good point, bringing up the 1948-1981 bond returns. Especially the 1964-1981 period shown in this chart:aeon wrote: So it is basically a 30/70 with a slight gold hedge, which seems to lower the volatility even more. Not a bad portfolio, but returns over the next 40 years are likely to be quite a bit lower, even if bonds do not enter an outright bull market. Found this concerning 48-81: http://awealthofcommonsense.com/real-ri ... portfolio/ Seems like real returns of 30/70 would have been close to flat over that time period? The gold would of course make up for some of the lost ground if that scenario were to become reality again.

[img width=500]http://awealthofcommonsense.com/wp-cont ... en-out.png[/img]

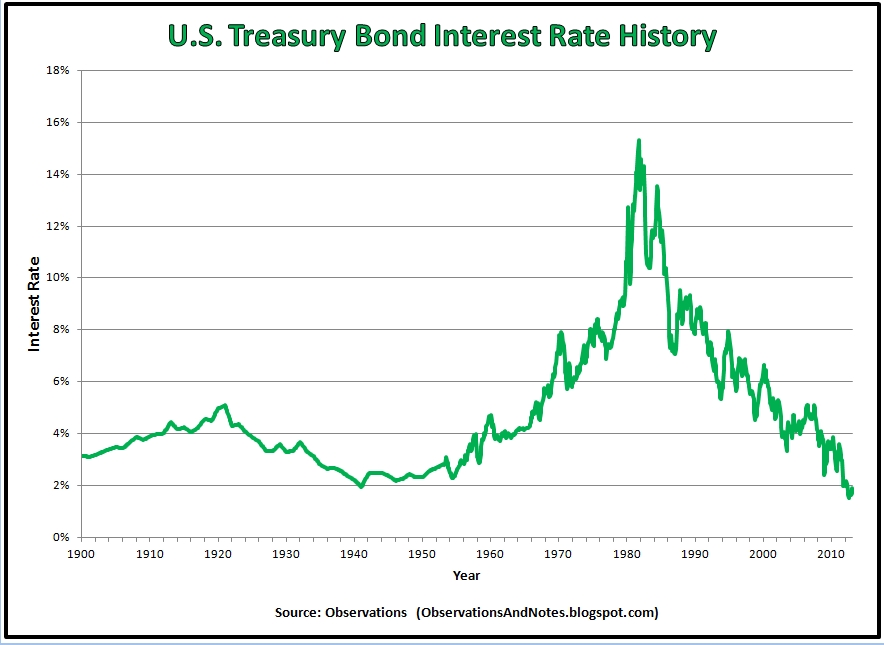

Obviously a bond-heavy portfolio is going to have a huge headwind in periods like that. And even the S&P 500 just barely beat the inflation rate. Gold would have helped in the late 70's. I haven't had a chance to find the data yet, but I suspect shorter treasuries and/or CD's would have outperformed 10 year treasuries in this period. With the rates rising rapidly in this period, shorter durations would, of course, have been preferable:

[img width=500]http://3.bp.blogspot.com/-Scat_VEIW9I/U ... istory.jpg[/img]

And even during the bond bull years, from 1980 to present, 10 year treasuries showed little advantage over 5 year. I'll look into this more.

But your point definitely stands: with bond yields at historic lows, and equity valuations high, future returns will likely be low.

I guess shorter maturities would hurt you in a depression era scenario though?

{kind=link}

{kind=link}