Pointedstick wrote:

[cross-posted from

http://gyroscopicinvesting.com/forum/pe ... #msg124921]

Most other portfolios inflate their returns by not having any cash, but in real life

nobody holds no cash; they simply don't count it as part of their investment portfolio. As a result, their investment portfolios are a smaller percentage of their net worth than a PP investor would have. So an apples-to-apples comparison of two people with identical net worths, one in the PP, and the other not, would either show that the PP person should have a higher amount of their money in the portfolio, or that the other portfolio should include all that cash off to the side.

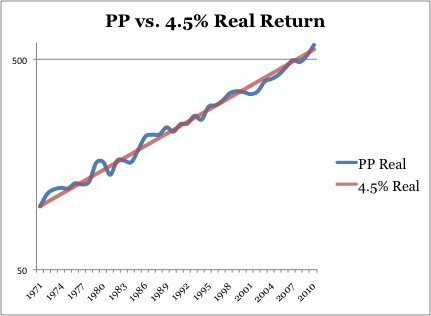

25% of total net worth being cash works out to 6.25 years living expenses, which is pretty reasonable. If we modify many conventional portfolios to have that much cash, the actual returns on the total portfolio value become much more comparable to the PP. For example, here's a standard 60/40 portfolio that's been modified to be 25% cash 75% 60/40. In other words, 25% cash, 45% stocks, 30% total bond market. PP in blue, other portfolio in red:

[img width=600]

http://i.imgur.com/9mNlCGa.png[/img]

The PP wins!

So no, you don't need a separate cash emergency fund if you invest with the PP.

to be honest i have rarely seen many people running conventional portfolio's that would tie up 25% in cash even in retirement . we keep a big cash position for our retirement model , 262k which represents 2 years withdrawals plus a 50k emergency fund and it is 13%. regardless of the amount the percentages most use stay in the range .

if i was collecting ss early it would be even less of a percentage.

if you visit the early retirement forum , one of the most popular forums around the median is 1-3 years . success rates are not effected by spending down from a conventional mix of equity and bonds even with zero cash .

withdrawal wise how much cash you keep is a comfort thing not a necessity as even spending down directly from 100% equity's has over a 90% success rate.

it makes little sense to deflate a conventional mix with 25% cash in your example as in practice that would just be an inefficient plan or an ultra conservative un-typical plan ..

the reason conventional plans do not need as much cash as the pp is conventional investing uses much higher equity positions so gains in the up cycles are much greater and they cushion the spending down of assets at a loss in the down years.

research by pfau , kitces and blanchett all came to the same conclusion , short of getting hit very bad the first few years of retirement ( which has happened only once in 111 rolling 30 year periods ) cash buffers do not add much value financially only mentally .

the pp never develops that extra cushion in most up cycles so its strategy counts on cash to fill the gaps . it is a strategy that works well by design but one that is unique to the pp.

i could lose 50% today , 27 years later and still be a head of the pp and that is with the below average returns the last 15 years making up for the first 15 years which were good . that brings the long term average back down to just the normal range .

interesting comparison but not a financially accurate one as it would be a comparison of a working strategy by design (the pp) against an investor mistake in planning out a portfolio or an exceptionally conservative one .

in fact by using a single premium immediate annuity ( spia ) even less cash is needed increasing success rates by a wide margin.

want even more guarantees with your conventional investing , spia's and permanent life insurance with more aggressive portfolio's have blown the doors off the typical buy term and invest almost 70% of every time frame run leaving both a higher amount of money for heirs and a higher income.

today more and more complex numbers crunching and research is showing successful retirement planning can be a whole lot more than just put together the pp or a conventional mix and have a nice life .

investing times have been anything but conventional and that may call for unconventional insurance products in all cases to help out .

today each one of us needs a strategy unique to us. many good planners today are running complex calculations doing age banding.

meaning allowing much higher withdrawals earlier in life and less as you age or in fact tailor it to your own life's events. maybe college for grand kids or weddings for them are off in the future and you want to incorporate that spending in the plan.

running simple charts may give you a ball park on sustainability historically but they mean little as far as an actual road map for a lifetime of spending dynamically and most important the GUARANTEE'S YOU MAY WANT and neither conventional portfolio's or the pp can do that alone .

that takes a combo of different insurance products plus your own investing to carry out.

yes you can have growth and comfort if you balance things right without hiding under a rock.

no one ever said do it yourself investing is going to be easy . it requires just as much skill and knowledge as any other skilled profession and simple answers to such complex issues are usually the wrong answers..

go to any retirement forum and you can witness the mistakes first hand as amatuers make decisons based on believing their own bull-sh%t , whether it is portfolio planning or when to take ss and all the ramifications that go with it .

and nooooo i don't work in the field nor have i ever . i am just open to learning and follow a lot of the new research on the subject .

{kind=link}