Page 1 of 1

Improving the PP through simplification

Posted: Fri Jan 30, 2026 9:09 am

by Kevin K.

Okay here's an out-of-left-field suggestion that came up on (of all places) the Bogleheads forums:

https://www.portfoliovisualizer.com/bac ... CMryVLBwXi

I guess you could call this "The Three Fund Portfolio" Harry Browne-style.

I see nothing but advantages here: you eliminate the tail risk of the 30 year Treasuries, have oodles of liquidity due to the cash-like nature of the short-term Treasuries and plenty of gold for SHTF insurance. Replacing the VTI with VT would make it into even more of a bunker. I mean if the PP is for money you can't afford to lose.....

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 10:22 am

by Smith1776

I would personally make it intermediate-term treasury bonds instead of short-term, but this is a perfectly valid approach too.

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 12:40 pm

by mathjak107

33% gold is more than i would want . i like gold but not that much

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 12:51 pm

by Smith1776

Agree with Mathjak

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 2:21 pm

by dualstow

I do like long bonds less than I did when I was younger. Even so, “simplifying” by removing them seems like simplifying one’s hand by lopping the thumb off.

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 2:40 pm

by Kevin K.

mathjak107 wrote: ↑Fri Jan 30, 2026 12:40 pm

33% gold is more than i would want . i like gold but not that much

It works even better with only 25% gold and more stocks - and trounces the regular PP even more thoroughly:

https://www.portfoliovisualizer.com/bac ... Krp1br6tiF

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 3:23 pm

by mathjak107

that i can see

Re: Improving the PP through simplification

Posted: Fri Jan 30, 2026 5:01 pm

by whatchamacallit

This is what I have been doing for a while now. 33% stocks, 33% treasury bills, 33% gold.

I got lucky and just rebalanced out of gold before the latest crash.

I believe it was the belangp videos that first got me comfortable with 33% gold with his 67% stocks, 33% gold allocation.

https://gyroscopicinvesting.com/forum/v ... hp?t=10777

The longer duration treasuries do back test better but that is from higher rates on the longer duration bonds.

I am not chaining myself to using treasury bills but plan on using the Swedroe 20 basis point rule that I see you posted about on bogle heads yourself. Thank you very much. I have it bookmarked.

https://www.bogleheads.org/forum/viewtopic.php?t=350803

The bonds need to make it worth it.

Re: Improving the PP through simplification

Posted: Sun Feb 01, 2026 3:00 pm

by seajay

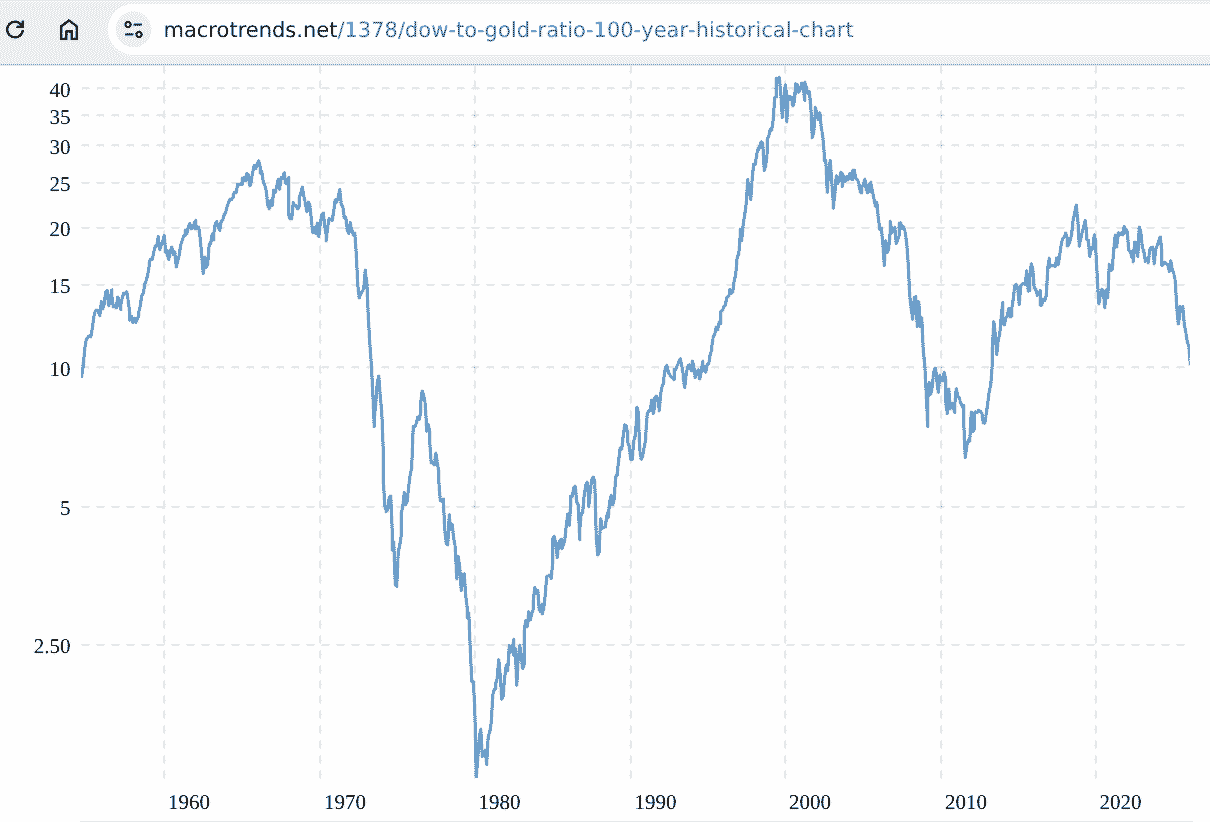

If you price in gold (as though it was money) rather than fiat dollars then historically the Dow price in ounces of gold ...

Do the same for T-Bills (accumulation) and CPI and both of those generally aligned with each other but in a generally downward slope manner, bought less gold (cost more dollars to buy gold) over time. Adding the dividends that the Dow provided to T-Bills made that downward slope more flat. Gold has more reflected M2 - debasement of dollars/debt expansion, which is increases faster than does CPI - that is slowed by productivity.

So generally gold, Dow (price only), T-Bills with the Dow dividends added might be considered as each broadly yielding flat lines (comparable to gold), but in varying volatility manner and where as the CPI downward slope line compared to just T-Bills alone that collective three way set > inflation. Yearly rebalancing and given historic wild extremes in volatility adds the potential to capture add-low/reduce-high 'trading' benefits. For instance in 1980 it cost a little more than a ounce of gold to buy a Dow stock index share, in 2000 it cost around 40 ounces (a single Dow share bought 40 ounces of gold).

The other main feature is that a combination of T-Bills perhaps with T Direct, physical gold in your possession and stocks held in a brokerage has more diverse counter party risk.

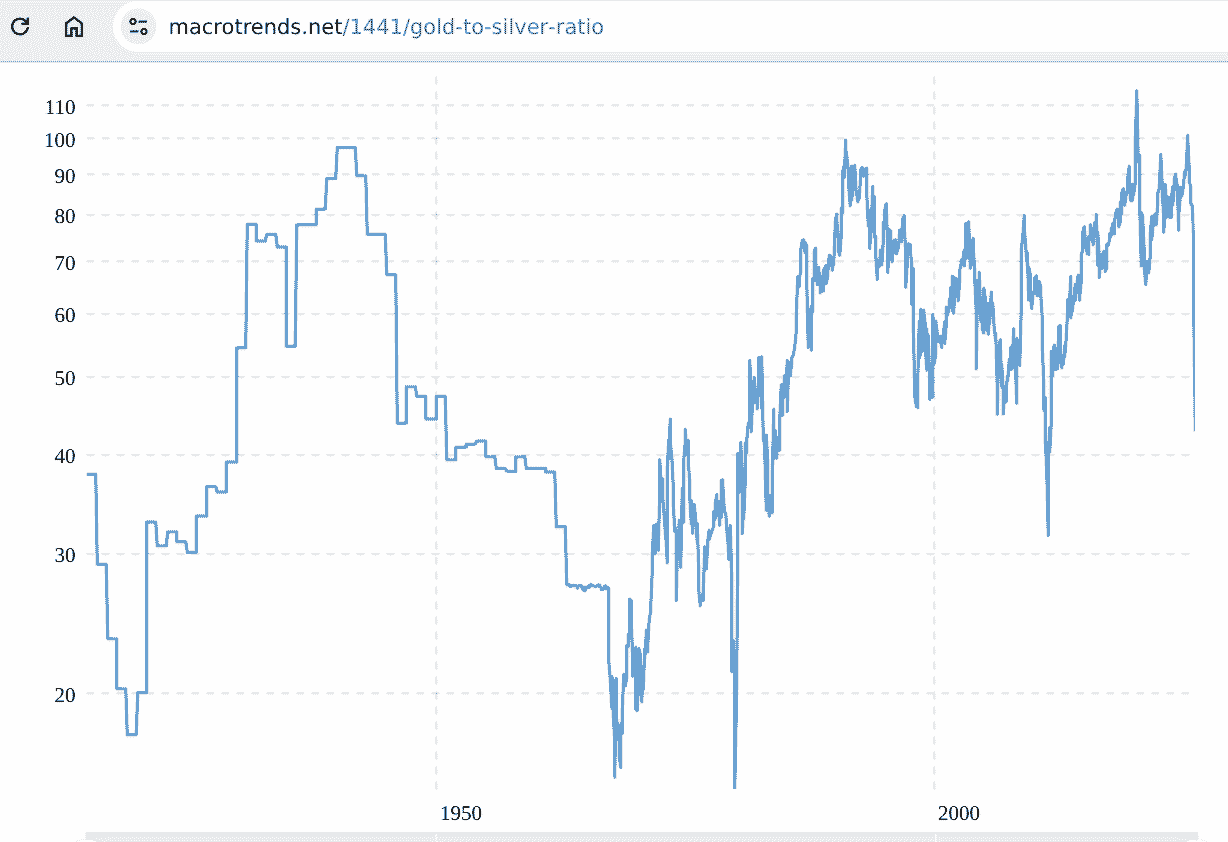

The relative stability of the baseline stock/gold/T-Bill asset allocation might be further worked to value-add (alpha), be more selective about 'bonds' (longer dated when yields are high/riskier or other alternatives/whatever); And/or perhaps swap out some gold for some silver when the gold/silver ratio is high and swap the silver back again to gold when the gold/silver ratio declines/is-low

Not long ago the gold/silver ratio was over 100, a ounce of gold bought 100 ounces of silver, more recently it has declined to around 50, the 100 ounces of silver you hold bought for a ounce of gold now buys two ounces of gold ... type 'trading'.

Yet another option is to transition to a more aggressive asset allocation as/when stock values are low (during/after deep dives), when the stock/gold/T-Bill asset allocation may have declined much less than stocks (buys perhaps twice as many stock shares than previously).

Optionality.

Re: Improving the PP through simplification

Posted: Tue Feb 03, 2026 6:41 am

by John34

Any thoughts on using Alpha Architect's CAOS ETF for like 50-90% of the Cash allocation? Its mutual fund version performed as desired in the COVID crash and it has beaten cash in up markets instead of bleeding money like other tail risk ETFs (eg Cambria's TAIL). Seems like an especially good idea in a taxable account since it doesn't throw off taxable income like cash.