Re: Ray Dalio on Bonds

Posted: Mon Oct 05, 2020 1:10 pm

Aren't you guessing by saying you don't want to hold them anymore?

Permanent Portfolio Forum

https://www.gyroscopicinvesting.com/forum/

https://www.gyroscopicinvesting.com/forum/viewtopic.php?t=11260

I think negative rates are unlikely. If you do get them, I can't imagine them being more than -.25% or -.5%. Anything more than that would be way too much stress on the financial sector and would force too many people towards alternative stores of wealth.AdamA wrote: ↑Mon Oct 05, 2020 12:56 pmWhat do you guys think the worse case scenario is for the Long Term Treasury market?mathjak107 wrote: ↑Sun Oct 04, 2020 5:38 am

this is why i said above we need to stop with the mental masturbation by reading what was or used to be , or how things may have back tested and concentrate on how things are reacting going forward .

driving and looking in the rear view mirror may not be a great idea .

If you can stomach 4 or 5 years of volatility, being in a 2:1 or 3:1 stock/gold allocation would probably provide you with much better "safety" while maximizing yields in regards to risk over the long-term.ahhrunforthehills wrote: ↑Mon Oct 05, 2020 3:16 pmI think negative rates are unlikely. If you do get them, I can't imagine them being more than -.25% or -.5%. Anything more than that would be way too much stress on the financial sector and would force too many people towards alternative stores of wealth.AdamA wrote: ↑Mon Oct 05, 2020 12:56 pmWhat do you guys think the worse case scenario is for the Long Term Treasury market?mathjak107 wrote: ↑Sun Oct 04, 2020 5:38 am

this is why i said above we need to stop with the mental masturbation by reading what was or used to be , or how things may have back tested and concentrate on how things are reacting going forward .

driving and looking in the rear view mirror may not be a great idea .

Again, keep in mind that gold is effectively a 0% treasury with no counter-party risk. Not to mention the long-term inverse correlation between stocks/gold is stronger than stocks/bonds. The only real downside is the spread.

But also keep in mind that your Uncle Sam has other options as well. If he hits zero at the long-end of the yield curve, he could just as easily create a 50 year or 100 year treasury to squeeze more juice out of it (albeit with diminishing results).

You could be telling your great-grandkids "I remember when 1,000 year treasuries were yielding 0.35%... those were the days!"

Would that make the PP still viable with ultra-long duration bonds? It does in theory.

However, if you take a look at that latest report from the Congressional Budget Office for the next 30 years... I think it would be obvious to a 4 year old that based on current yields and future expenditures... holding Long-Term Treasuries over the long term is pretty crazy. Another industrial revolution wouldn't be enough to get America out of our hole. You are staring down the barrel of either default or hyperinflation.

I am only aware of one leader who was able to effectively bring his people out of a mountain of debt, made sure his people were well fed, provided lots of social programs, and boosting wages more than double that of other leading nations. His people loved him. The guy was a German named Adolf.

Even if this happened in america, I suspect rates will rise BEFORE we start brutally robbing people in other countries.

So obviously ultra-long duration bonds start really walking up that risk curve. How much risk is really dependent on how things play out over the rest of your life.

The PP has short-term volatility. I suspect it will be a dog performance-wise in the future. You can either go with the dog or extend the length of that short-term volatility. If you can stomach 4 or 5 years of volatility, being in a 2:1 or 3:1 stock/gold allocation would probably provide you with much better "safety" while maximizing yields in regards to risk over the long-term.

Obviously, if you are near retirement, you do not necessarily have that luxury of 4 to 5 years of volatility. At which point, you would want to look towards shorter duration bonds (like mathjak has done).

Sorry, I should have been more clear.... and I actually just realized I made a bad typo. I meant 1:2 or 2:3 allocation.modeljc wrote: ↑Mon Oct 05, 2020 4:06 pmIf you can stomach 4 or 5 years of volatility, being in a 2:1 or 3:1 stock/gold allocation would probably provide you with much better "safety" while maximizing yields in regards to risk over the long-term.ahhrunforthehills wrote: ↑Mon Oct 05, 2020 3:16 pmI think negative rates are unlikely. If you do get them, I can't imagine them being more than -.25% or -.5%. Anything more than that would be way too much stress on the financial sector and would force too many people towards alternative stores of wealth.AdamA wrote: ↑Mon Oct 05, 2020 12:56 pmWhat do you guys think the worse case scenario is for the Long Term Treasury market?mathjak107 wrote: ↑Sun Oct 04, 2020 5:38 am

this is why i said above we need to stop with the mental masturbation by reading what was or used to be , or how things may have back tested and concentrate on how things are reacting going forward .

driving and looking in the rear view mirror may not be a great idea .

Again, keep in mind that gold is effectively a 0% treasury with no counter-party risk. Not to mention the long-term inverse correlation between stocks/gold is stronger than stocks/bonds. The only real downside is the spread.

But also keep in mind that your Uncle Sam has other options as well. If he hits zero at the long-end of the yield curve, he could just as easily create a 50 year or 100 year treasury to squeeze more juice out of it (albeit with diminishing results).

You could be telling your great-grandkids "I remember when 1,000 year treasuries were yielding 0.35%... those were the days!"

Would that make the PP still viable with ultra-long duration bonds? It does in theory.

However, if you take a look at that latest report from the Congressional Budget Office for the next 30 years... I think it would be obvious to a 4 year old that based on current yields and future expenditures... holding Long-Term Treasuries over the long term is pretty crazy. Another industrial revolution wouldn't be enough to get America out of our hole. You are staring down the barrel of either default or hyperinflation.

I am only aware of one leader who was able to effectively bring his people out of a mountain of debt, made sure his people were well fed, provided lots of social programs, and boosting wages more than double that of other leading nations. His people loved him. The guy was a German named Adolf.

Even if this happened in america, I suspect rates will rise BEFORE we start brutally robbing people in other countries.

So obviously ultra-long duration bonds start really walking up that risk curve. How much risk is really dependent on how things play out over the rest of your life.

The PP has short-term volatility. I suspect it will be a dog performance-wise in the future. You can either go with the dog or extend the length of that short-term volatility. If you can stomach 4 or 5 years of volatility, being in a 2:1 or 3:1 stock/gold allocation would probably provide you with much better "safety" while maximizing yields in regards to risk over the long-term.

Obviously, if you are near retirement, you do not necessarily have that luxury of 4 to 5 years of volatility. At which point, you would want to look towards shorter duration bonds (like mathjak has done).

What is 2:1 allocation? 50% stock and 25% Gold? 25% cash or short duration bonds like SHY?

I was inspired by this tweet: https://twitter.com/alexisohanian/statu ... 7427155970. I interpreted "alternative" as "real estate"

Food for thought....senecaaa wrote: ↑Tue Oct 06, 2020 6:43 amI was inspired by this tweet: https://twitter.com/alexisohanian/statu ... 7427155970. I interpreted "alternative" as "real estate". No theory behind it.

got stopped out already ...

Hold the phone. Home loans get massively cheaper as yields drop, no? You simply get a lot more for your money.

Seriously?? Can the landlord evict the tenant, or will the government pay the landlords bank loan if they have oneahhrunforthehills wrote: ↑Tue Oct 06, 2020 9:09 am Sorry, one more... government has made it very clear lately that people don’t have to pay their rent if they lack emergency savings. Uncle Sam basically said real estate investors will be the first to be sacrificed during tough economic periods.

That definitely has to change the correlation dynamic between stocks and real-estate going forward.

Simonjester wrote: evictions are suspended, and outside what ever small business assistance is left over after big business sucked most of it up, is all they have. Property management is a whipping boy for the left, all rent is evil capitalism and slumlord-ism to them ..

I think what you're talking about matters when discussing your own home's price, but not owning and operating real estate like a business like REITs do. REITs and other real estate investors can use low rates right now to secure the productive asset (the actual real estate), and can then respond to market conditions in whatever ways they need to. If inflation goes up and people start earning higher wages, they can raise the rent. If people don't want to live/work there, they can improve the property. If they can't get enough rent to be profitable, they can defer maintenance and let the property quality slide.ahhrunforthehills wrote: ↑Tue Oct 06, 2020 8:55 am Hold the phone. Home loans get massively cheaper as yields drop, no? You simply get a lot more for your money.

18.45% Rate (Oct 1981) vs 3% (Now) on $300k 30 year fixed rate:

$4,632 vs $1,265 per month for the SAME EXACT HOUSE.

The average home has gotten much larger because people have more spending power to throw at houses (and because builders can now make your trim out of cardboard.

Here is the question:

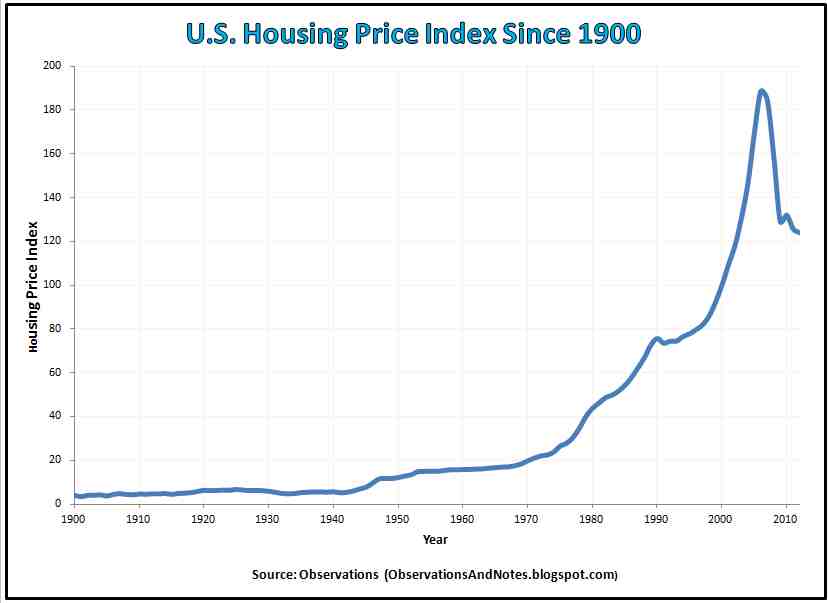

Did real estate do just as well from 1941 to 1981 (rising rates) as it did from 1981 to 2021 (falling rates):

Not even close.

It appears you are jumping from the Titanic into a lifeboat... but the lifeboat is welded to the deck of the titanic.

If (when) interest rates go up... the monthly price of an existing 5,000 sqft house goes up as well. Now you have fewer buyers. Since houses have gotten bigger (the bigger the house the more they cost to maintain) and they use less quality materials (increasing costs of repairs) the financial needs will be higher yet.

It reminds me of the best days of owning a boat.. the day you buy it and the day you sell it. When rates are falling everybody “has gotten a good deal on a new home”. But you are still talking about a pile of sticks sitting out in the rain. It doesn’t get better with age.

Also keep in mind other factors that have historically inflated real estate sales. Having a 20% down payment was the minimum many years ago. However, the time period you are backtesting is a period where people were able to put much much less down (which increases the risk like crazy).

Part of this is because banks have an incentive to push loans in a falling rate environment. If they need to repo your house, the falling rates help ensure they can resell the house easily.

Are there other factors at play outside of rates? Probably. But I am not seeing anything that makes me feel warm and fuzzy...

Today’s younger generation’s value system doesn’t seem to circle around nice houses like earlier generations. They would rather have expensive coffee and peletons.

Also, the largest population growth going forward is the hispanic population. They are much more likely as a group to have multiple families living in the same house.

You also have the downward pressure of the baby-boomers downsizing, selling, etc.

Housing is also arguably in a larger bubble than it was during the last collapse:

https://gordcollins.com/wp-content/uplo ... istory.png

Lastly, the chances of budget shortfalls in the future are enormous (again, refer to the CBO report). Higher property taxes seem inevitable.

The only plus I can think of is that you still get tax incentives through depreciation on the business side of it. However, if Trump ever has his tax returns exposed... those deductions could be a political unpopular issue going forward.

I know Im a little late to the party here. But from a systematic perspective, wouldn't it make more sense to look at indicators that actually signal a bond reversal instead of just selling because rates are low and buying because they are high? What defines the subjective terms "low" and "high"? I mean selling into falling rates has been a widow maker trade for decades now. Why would that suddenly change today of all days? Why not look for indicators like rising inflation, growth, volatility, or yields as a means to sell, instead of selling because rates are falling and they are making you too much money? This is what I would look at if I were trying to create a systematic bond allocation. Those are the actual stats worth looking at for a leading indicator of what bonds will do going forward. Right now inflation and growth are non existent, bond volatility is super low, and rates are staying surprisingly stable considering the massive stock rally we have had over the last few months. It's kind of hard to argue for the death of the bond bull market and truly justify systematically selling bonds with all 4 of those stats saying the opposite.ahhrunforthehills wrote: ↑Thu Sep 24, 2020 12:10 pm

What I am getting at is have a documented mechanism in place to allocate out of LTT as yields decline, and back in as LTT yields go up... otherwise your emotions can easily get you lost at sea going forward.

+1pmward wrote: ↑Tue Oct 13, 2020 1:09 pm I know Im a little late to the party here. But from a systematic perspective, wouldn't it make more sense to look at indicators that actually signal a bond reversal instead of just selling because rates are low and buying because they are high? What defines the subjective terms "low" and "high"? I mean selling into falling rates has been a widow maker trade for decades now. Why would that suddenly change today of all days? Why not look for indicators like rising inflation, growth, volatility, or yields as a means to sell, instead of selling because rates are falling and they are making you too much money? This is what I would look at if I were trying to create a systematic bond allocation. Those are the actual stats worth looking at for a leading indicator of what bonds will do going forward. Right now inflation and growth are non existent, bond volatility is super low, and rates are staying surprisingly stable considering the massive stock rally we have had over the last few months. It's kind of hard to argue for the death of the bond bull market and truly justify systematically selling bonds with all 4 of those stats saying the opposite.

I think we are talking about apples and oranges here.pmward wrote: ↑Tue Oct 13, 2020 1:09 pmI know Im a little late to the party here. But from a systematic perspective, wouldn't it make more sense to look at indicators that actually signal a bond reversal instead of just selling because rates are low and buying because they are high? What defines the subjective terms "low" and "high"? I mean selling into falling rates has been a widow maker trade for decades now. Why would that suddenly change today of all days?ahhrunforthehills wrote: ↑Thu Sep 24, 2020 12:10 pm

What I am getting at is have a documented mechanism in place to allocate out of LTT as yields decline, and back in as LTT yields go up... otherwise your emotions can easily get you lost at sea going forward.

I would have to answer your question with a question:pmward wrote: ↑Tue Oct 13, 2020 1:09 pm

Why not look for indicators like rising inflation, growth, volatility, or yields as a means to sell, instead of selling because rates are falling and they are making you too much money? This is what I would look at if I were trying to create a systematic bond allocation. Those are the actual stats worth looking at for a leading indicator of what bonds will do going forward. Right now inflation and growth are non existent, bond volatility is super low, and rates are staying surprisingly stable considering the massive stock rally we have had over the last few months. It's kind of hard to argue for the death of the bond bull market and truly justify systematically selling bonds with all 4 of those stats saying the opposite.

The net interest to service the debt is pretty crazy when you look at their projections. Some people will argue that those are just "projections" and not reality. True. They do not calculate in anything else going wrong over the next 30 years or any other Covid-related relief packages.Federal debt held by the public is projected to increase to 98 percent of gross domestic product (GDP) at the end of this year, up from 79 percent of GDP in 2019 and 35 percent in 2007, before the start of the previous recession.

In our projections, debt continues to rise, reaching 195 percent of GDP by 2050, far exceeding the previous high of 106 percent recorded just after World War II.

How soon is action required?

There is no set tipping point at which a fiscal crisis becomes likely or imminent, nor is there an identifiable point at which interest costs as a percentage of GDP become unsustainable. But as the debt grows, the risks become greater.

{kind=link}