1980 was a great start year for stocks, a (very) bad start year for gold. That aside and start 1980 with 50/50 stock/gold, where you left that as-is but looked to deploy gold into stock when stocks dipped, and at the end of 1987 might have been selected as the time to do that. Stocks and gold tend to have multi-year inverse correlations so as stocks dip -25% so gold might spike +33% and vice-versa ... type concept. How did 50/50 stock/gold from the start of 1980 to end of 1987 and then all-stock thereafter compare to 100% stock from the start of 1980? Well all-stock achieved a 11.2% annualized nominal, 7.8% real, whereas the initial stock/gold 50/50 ended up with 0.96% annualized less (so 10.2% nominal, 6.9% real). $707K final/recent ($10K initial) instead of a little over a $1M for all-stock. Still not a shabby outcome for a bad case.

What if no migration of gold into stocks occurred, well non rebalanced stock/gold ended more recently with $554,246, compared to $1,073,524 for all-stock. 6.2% real vs 7.8% real.

Whilst it could have been different in other cases, such as start with $10 in 2000 and all-stock 10.4% annualized nominal, 7.6% real. 50/50 initial stock/gold and deploying gold into stock at the end of 2002 ... 12% nominal, 9.2% real. Or for a 1972 start date, rotating gold into stock at the end of 1974, and 1972 to recent 8.73% annualized real, compared to 6.23% annualized real for all-stock from 1972.

Many underestimate the optionality of cash (gold) Buffett views cash as a Call Option without a Expiration Date or a Strike Price, the value of which can earn when he acquires other assets at bargain prices. The cost of carrying that can be relatively low/acceptable, 1980 type bad case start date for example, where rewards are still 'satisfactory'. Such hedging is inclined to reduce the upside great case outcome (but can still yield greater rewards than all-stock from the get-go), but also tends to reduce the worst case outcome, which for some/many may be the priority.

What Buffett further does is to not only buy when stocks have pulled-back, but also buy into the more depressed sector, selecting the more depressed stock in that sector, and for him ideally buys the controlling interest in that stock, as, as the owner, capital can be freely moved between his different businesses. But not exclusively. I note that whilst Buffett bought a lot of Apple shares in recent years, he has spent around twice as much on buying another single stock that largely hasn't received anywhere near as much media attention. Which stock? Why BRK (share buybacks) of course. On a measure of 67/33 BRK/APPL stocks since 2016 to recent ... that's grown at a near 21% annualized real rate of return

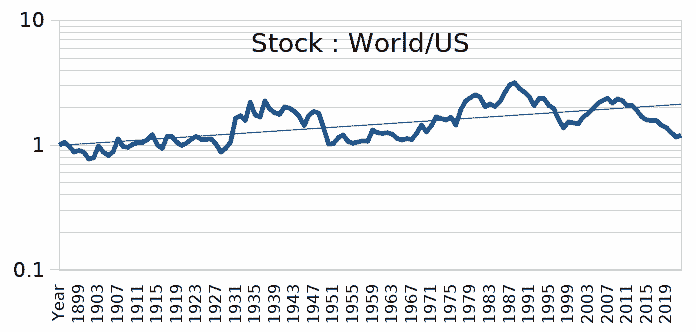

PV