Asset class with high correlation to LTT’s?

Moderator: Global Moderator

Asset class with high correlation to LTT’s?

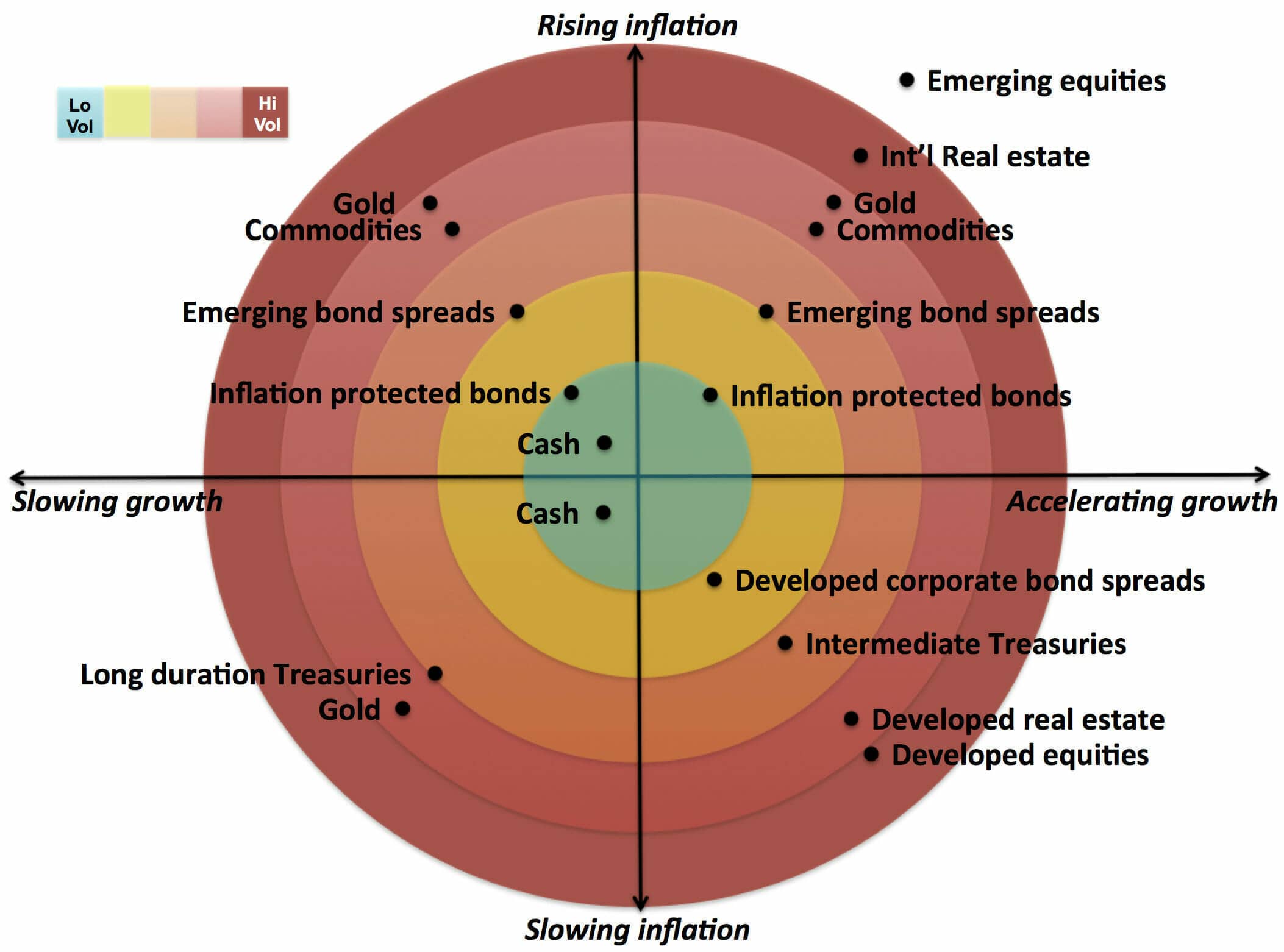

Does anyone know of an asset class that correlates strongly with LTT’s. Like a lot of people in the forum, LTT’s at zero scare me and I want to figure out a way to keep my portfolio dynamics the same while reducing my exposure to LTT’s.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Asset class with high correlation to LTT’s?

there really is nothing except holding way more intermediate term bonds or inflation adjusted

-

boglerdude

- Executive Member

- Posts: 1317

- Joined: Wed Aug 10, 2016 1:40 am

- Contact:

Re: Asset class with high correlation to LTT’s?

They're not at zero.

Re: Asset class with high correlation to LTT’s?

Quick question: Is the asset class you are trying to find ideally supposed to be essentially something that has the punch and firepower (in terms of appreciating heavily and quickly) when stocks plummet like they did in 1974, 1987, the summer of 1998, various times in 2000 and 2001, 2002, 2008, and early 2020....but that has none of (or at least less of) the interest rate risk of LTTs? I think I might have a blend of assets that might work for you (although be warned: In times when equity markets are fairly steady but rates are flat or falling this blend of assets will not appreciate nearly as much as good old regular LTTs will...although conversely, in times of rising rates it also lacks much of the duration risk that LTTs have). Is this what you are looking for?

Re: Asset class with high correlation to LTT’s?

D1984 - throw out what you have please. I’m interested. But I remembered the LTT’s are a deflation hedge that will still work for that purpose. I guess the only thing they are now less of a hedge against is an economic contraction.

Re: Asset class with high correlation to LTT’s?

Thanks Mathjak. Been reading your posts on the Ray Dalio thread.mathjak107 wrote: ↑Fri Nov 06, 2020 3:49 am there really is nothing except holding way more intermediate term bonds or inflation adjusted

-

ahhrunforthehills

- Executive Member

- Posts: 326

- Joined: Tue Oct 19, 2010 3:35 pm

Re: Asset class with high correlation to LTT’s?

Unfortunately, there is no way to keep your current portfolio dynamics exactly the same. You can't change one factor without changing all of the other factors.

You might find this helpful if you haven't seen it yet: https://www.listenmoneymatters.com/wp-c ... eather.jpg

{kind=link}

Basically, gold is likely the answer... albeit it with a longer draw-down duration. Gold is basically a 0% bond with better counter-party risk.

Obviously, adding more gold would change your dynamic even more. You would need to offset it with more stock. Here is a video that crunched some data: https://www.youtube.com/watch?v=LA2Yr6NoZyA

Let me also point out that even if you COULD keep your investing dynamic the same... is the investing environment still compatible with that dynamic? Or in other words, do you really need to turn on your sprinklers if it is raining outside?

What I am getting at is the deeper we dive into a Modern Monetary Theory world, the less portfolios like the PP may actually matter.

The "portfolio dynamic" for which you (and all of us) seek is one that will bet on prosperity while hedging against collapse (and re-balance accordingly). You are basically using Long Term Treasuries as insurance to bail you out of a market crash.

However, in an MMT environment, isn't someone already doing this for you?

Basically, if the market crashes, the government supports the market (i.e re-balances) by borrowing money (i.e. LT Bonds) from the future. This borrowed money makes its way into equities though helicopter money, low-interest loans that lead to stock buybacks, infrastructure projects, etc.

When the market is good (i.e. full-employment, etc.) the government re-balances back. Asset rebalancing manually for “safety” purposes might very well be a waste of time (and certainly a waste from a tax perspective).

So perhaps the real question is, does the performance you receive from moving in and out of bonds in a PP make up for the risk and capital destruction that occurs through re-balancing?

When you shift from a free capital market to that of MMT, the earth has shifted under your portfolio's feet. In a lot of ways, perhaps the model has been greatly simplified. In this new world, the government would now have a simple lever that varies from "Booming Market & High Inflation" to "Market Crash & No Inflation". It wouldn't take a genius to figure out where that throttle spends most of its time when you are talking about elected officials.

This type of world would certainly require you to purchase a lot less LTT.

Re: Asset class with high correlation to LTT’s?

OK, but keep in mind that NONE of this is anywhere near traditional PP so if you replace any long bonds with these assets you've effectively "broken" the PP and who knows how it will work going forward:

Here is what I was thinking of if you simply wanted a "stuff that will likely do about as well (or better) than LTTs when stocks are plummeting but don't have (or at least don't have so much of) the interest rate risk:

1. Long-short ETFs that go long one factor that will do well during times of market crises while going short another that will likely do poorly during times of market crises. Examples of these have the ticker symbols BTAL and MOM. These ETFs have only existed since late 2011 but the underlying indexes have existed since 1-1-2002 (and in fact I have the data for the index underlying BTAL daily all the way back to that date; S&P Dow Jones now runs these indexes and could probably get you the monthly data for the index underlying MOM if you emailed and asked for it). BTAL goes short high-volatility stocks and long-low volatility ones; MOM goes short low momentum stocks and long high momentum ones; both of these ETFs take advantage of two tendencies:

First, the tendency of negative momentum stocks and high volatility/high beta stocks to do worse than the market as a whole during crashes,

Second, the well-known anomaly of low-beta/low-vol stocks to do better than high-beta stocks (the "betting against beta" anomaly) and the proven tendencies of stocks with positive price momentum to continue outperforming (the momentum effect).

Note that both of these ETFs are true market neutral and NOT sector bets (low-vol ETFs are heavier in utilities and consumer staples than the overall market and momentum ETFs are heavier in tech and consumer discretionary than the overall market) like traditional "low beta" or "momentum" ETFs like SPLV or MTUM; IIRC the BTAL and MOM ETFs are weighted so that their underlying sector composition is as close to the overall S&P 500 as possible but within each of those sectors they go long the low-beta (in the case of BTAL) or high positive momentum (in the case of MOM) stocks and short the high-beta (in the case of BTAL) or high negative price momentum (in the case of MOM) stocks.

Given the existence of the "betting against beta" and "momentum" factor anomalies both of these ETFs probably have a (small) positive expected long-term return (albeit maybe only 0.5% to 1% nominal a year) rather than a negative return.

2. A pure short ETF (or mutual fund) combined with enough lower-duration bonds that this slice of the portfolio won't lose as much as simply replacing 100% of the LTTs with a pure short fund would. FWIW if I had to choose a pure short fund to use in a strategy as above it would probably be DWSH given the backtested (and live) results of it this fund seems to have about the same StDev as a 50/50 mix of a 3X daily short S&P 500 ETF and a 2X daily short S&P 500 ETF but with slightly higher performance in bear markets without nearly the downside in bull markets.

3. A tail-risk hedge ETF like TAIL (which itself has an underlying portfolio made up of roughly 90% 8-10 year Treasuries and 10% put options on the S&P 500) mixed with some lower-duration Treasuries as in the portfolio referenced in section 2 above.

4. A trend-following fund like MFTNX; this fund bets on trends in commodities, interest rates, currencies, bonds, stock markets (both US and intl), etc and the underlying strategy (a strategy called WMA from a company called Dunn Capital) has returned roughly 14% a year since inception back in the mid-1970s; note that MFTNX did not use the Dunn Capital strategy until 10-1-2015 so any results before then do not reflect the performance of the current strategy of this fund; Dunn Capital will be glad to send you a spreadsheet showing returns of their strategy monthly (as an SMA) since inception if you want to backtest performance of MFTNX before autumn 2015. Also, please remember that Dunn Capital WMA is NOT designed specifically as a "do well when the markets do poorly" strategy like TAIL, DWSH, BTAL, or MOM is but rather aims to be completely uncorrelated with stock/bond/gold markets (i.e. a correlation close to 0 over the long term); as such there may be times (like 1981 or 2018) when it does poorly when the market also is down or when the market is flat (like 1994) but also times it will do very well when the market is down (crash of 1987, 1990, 2000-2002, 2008, 1Q 2020) or flat (2011, 2015); times when it will do kind of meh or even do poorly despite stock markets being up (1976, 1985, 1988, 1992, 2003-2005, 2012), and times when it will do well or stunningly well despite stock markets also being up (1979, 1980, 1983-84, 1993, 1995-1999, 2010-2011, 2013-2015, 2017, 2019).

5. A blend of very-short term STTs (like SHY or VFIRX) combined with a 2X or 3X daily ITT fund like UST or TYD; there was some discussion of Bogleheads a few months back (I wish a could find the thread) about replacing TLT/EDV/VUSTX with just such a blend in a portfolio; based on backtesting of these ETFs back to the 1960s it seemed to have similar upside as LTTs but with less downside during periods of rising rates (which makes sense given how daily leveraged ETFs work; they will do better than the underlying in a steadily rising or steadily falling market and will only do worse in a choppy but overall flat market).

6. An annually or quarterly rebalanced "barbell" portfolio consisting 90% or 95% of a blend of safe assets like high-yield savings accounts, EE savings bonds, I-bonds, and short-term and intermediate-term TIPS with a small amount of assets that are essentially leveraged bets on rates continuing to fall and thus on long Treasuries doing well (The ETF TMF, options on 30-year Treasuries, 30-year Treasury futures). This portfolio is more or less an attempt to take advantage of higher-than-market guaranteed rates (savings accounts pay more than T-bills; I-bonds and EE bonds have some unique "heads I win tails Uncle Sam loses" that regular marketable bonds simply don't have) on certain unique safe instruments while participating in most of the upside if LTTs do rally while having very little of the downside if LTTs fall sharply due to a rise in rates.

Re: Asset class with high correlation to LTT’s?

ahhrunforthehills wrote: ↑Sun Nov 08, 2020 10:20 amUnfortunately, there is no way to keep your current portfolio dynamics exactly the same. You can't change one factor without changing all of the other factors.

You might find this helpful if you haven't seen it yet: https://www.listenmoneymatters.com/wp-c ... eather.jpg

Basically, gold is likely the answer... albeit it with a longer draw-down duration. Gold is basically a 0% bond with better counter-party risk.

Obviously, adding more gold would change your dynamic even more. You would need to offset it with more stock. Here is a video that crunched some data: https://www.youtube.com/watch?v=LA2Yr6NoZyA

Let me also point out that even if you COULD keep your investing dynamic the same... is the investing environment still compatible with that dynamic? Or in other words, do you really need to turn on your sprinklers if it is raining outside?

What I am getting at is the deeper we dive into a Modern Monetary Theory world, the less portfolios like the PP may actually matter.

The "portfolio dynamic" for which you (and all of us) seek is one that will bet on prosperity while hedging against collapse (and re-balance accordingly). You are basically using Long Term Treasuries as insurance to bail you out of a market crash.

However, in an MMT environment, isn't someone already doing this for you?

Basically, if the market crashes, the government supports the market (i.e re-balances) by borrowing money (i.e. LT Bonds) from the future. This borrowed money makes its way into equities though helicopter money, low-interest loans that lead to stock buybacks, infrastructure projects, etc.

When the market is good (i.e. full-employment, etc.) the government re-balances back. Asset rebalancing manually for “safety” purposes might very well be a waste of time (and certainly a waste from a tax perspective).

So perhaps the real question is, does the performance you receive from moving in and out of bonds in a PP make up for the risk and capital destruction that occurs through re-balancing?

When you shift from a free capital market to that of MMT, the earth has shifted under your portfolio's feet. In a lot of ways, perhaps the model has been greatly simplified. In this new world, the government would now have a simple lever that varies from "Booming Market & High Inflation" to "Market Crash & No Inflation". It wouldn't take a genius to figure out where that throttle spends most of its time when you are talking about elected officials.

This type of world would certainly require you to purchase a lot less LTT.

Thanks! Very helpful. Plus now, thanks to you, I learned about Belangp

Re: Asset class with high correlation to LTT’s?

D1984 - thanks! I need to print this one out and reread carefully.