Thanks for starting this topic, Desert. Believe it or not, after researching simple investing options for my in-laws I was considering launching the same discussion for the exact same portfolio idea. I know VWIAX has historically been somewhat popular here, so I think many people will find the idea valuable.

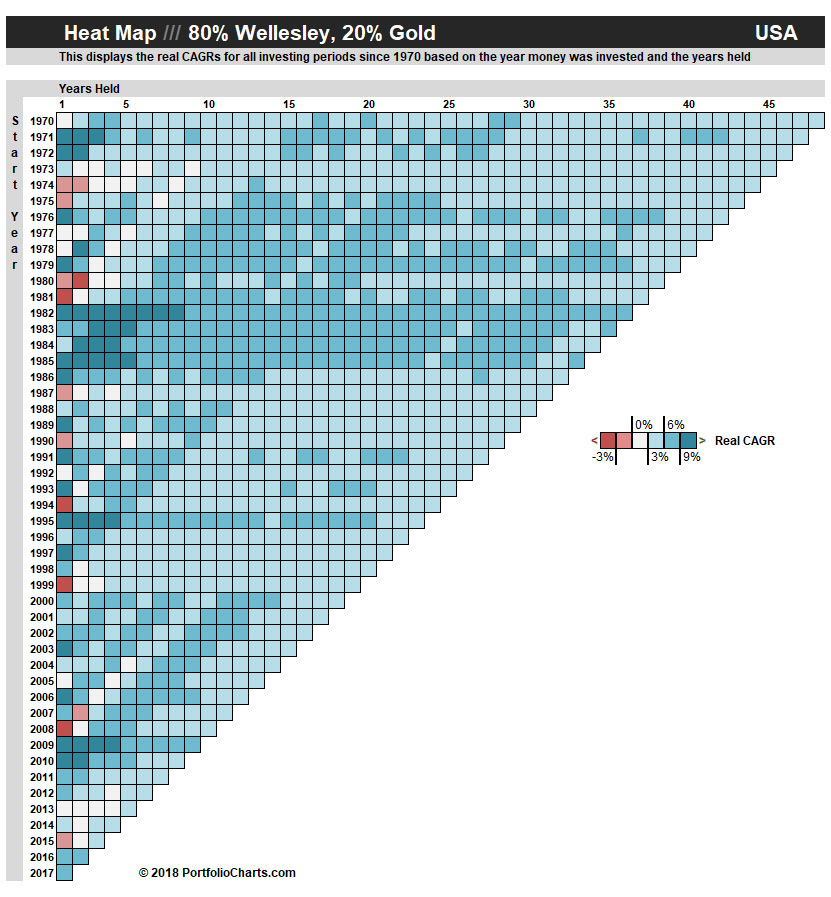

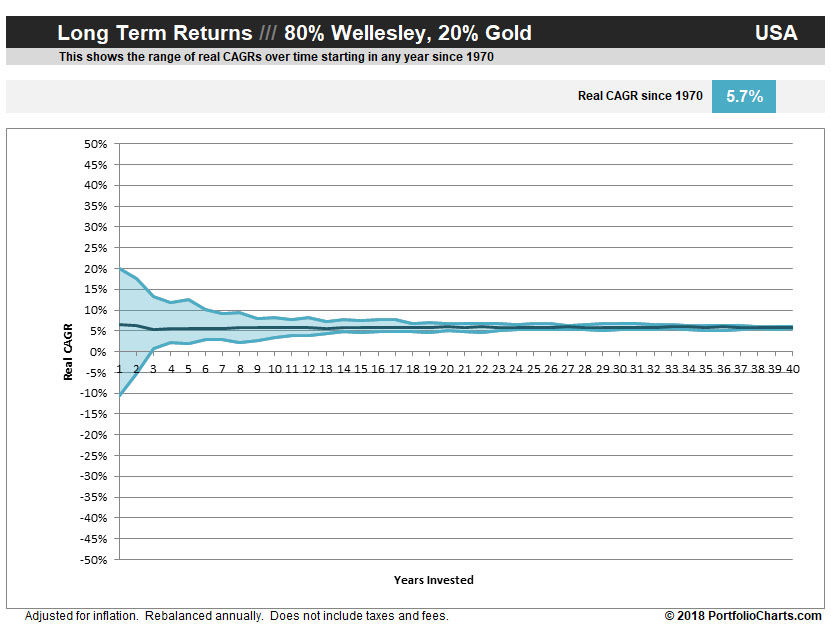

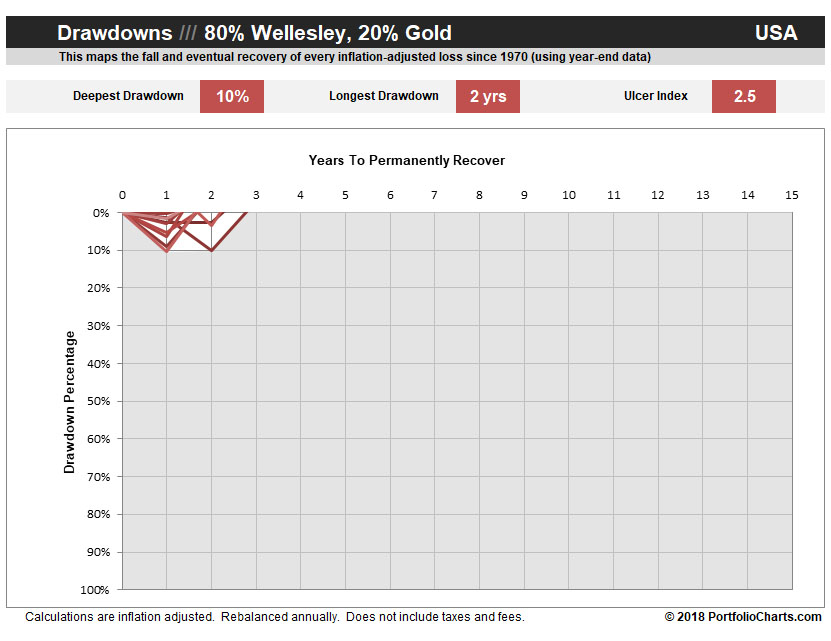

Long story short -- you're exactly right that the 80/20 Wellesley/Gold portfolio has historically been very competitive with the Golden Butterfly. The returns were about half a percent lower on average, but the overall performance was equally consistent with similarly manageable drawdowns. IMHO, anyone interested in a very simple high-quality and hands-off asset allocation would do just fine putting their money in VWIAX and buying some gold on the side.

I use short term treasuries instead of Tbills for the GB. I imagine that makes up part of the difference, although you should note that the Simba spreadsheet will never perfectly match my numbers as we use different data sources these days.

No Wellesley on Portfolio Charts at the moment, but I have plenty of my own tools to play with. Let me know if you have a specific request and I'll see what I can do.

Although to make it more fair, shouldn't at least some cash (5%?) be included in Wellesley+Gold? Can't imagine being retired without some cash.

I do own some Wellesley - good for what it is. I'd be worried going all in on LCV and. Corporage bonds. I'd also look at Global Wellesley -- Intl as well as US value stocks.

[Edit for multiple typos]

Last edited by Dieter on Sat Jun 09, 2018 11:43 am, edited 1 time in total.

I remember Medium Tex proposing something very similar back in the epic Bogleheads thread. I don't exactly remember how much gold he was talking about - maybe 10%, but I think that was based more on the idea that people who are looking for simple might be skittish about holding more gold than that.

I had the same reservations as Dieter though: With the GB (or PP for that matter), your cash savings counts as part of the cash allocation, and it's there to fund your living expenses during a drawdown. With a non-cash portfolio, you will still end up holding some cash, because nobody likes bouncing checks or selling investments at a loss. Not counting that cash as part of the allocation artificially inflates the expected returns.

We've had discussions on this in the past and definitely it's time for another one!

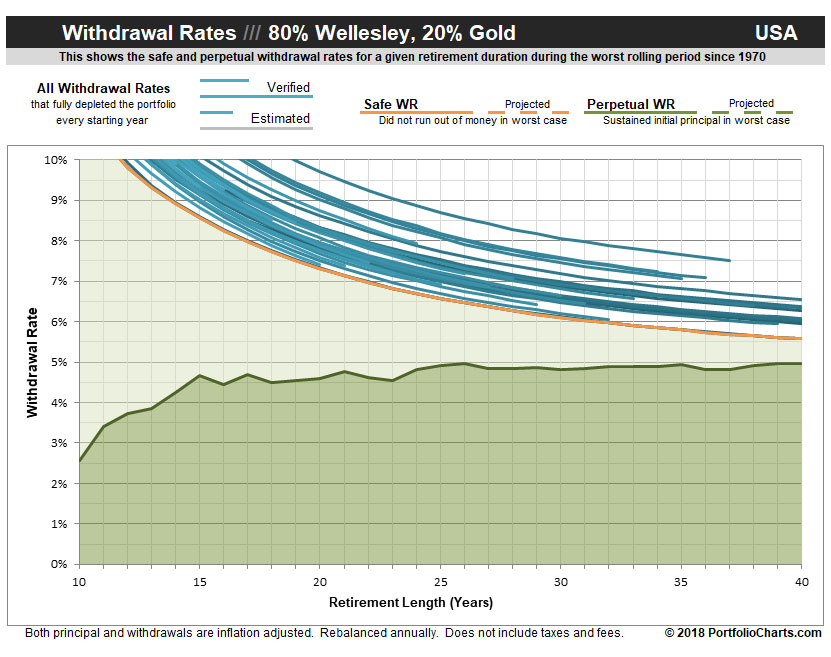

Starting with your example: Let's assume that you're just starting retirement, and your portfolio is exactly 25x annual expenses, i.e. expenses are 4% of the portfolio size. So your 2% assumes that you keep no more than 6 months expenses in cash. That seems a bit thin and I personally wouldn't be comfortable with that. This cash is not just for routine expenses, it's also for things like financing a new roof or an unforeseeable medical incident, and also to ride out market corrections. Most people probably head into retirement with at least 1 year in cash (4%), and many financial advisor/gurus recommend 5 years (20%). Notice that at the 5 year level, you are talking quite a significant slice of the portfolio.

Maybe it's mathematically better to stay invested at all times and sell as needed, but I kinda doubt it. I ran some simulations once, and there are definitely CAGR penalties for selling too often, or during a downturn. There's also the sleep at night factor. Skimping on cash works better if your portfolio is significantly more than 25x expenses, but if you're right at that 4% edge, I don't think you can afford it.

Wellesley really looks like it uses some kind of trend-following risk management. The ascent over the decades is so clean, the drawdowns shallower than a 60/40. I'll wager there is effectively 1/4 - 1/2 trend-following in the investment policy, even if that terminology isn't used. These practices have been known for a long time.

It depends how often you have to sell assets during a drawdown. The math gets really nasty when that happens:

Starting portfolio = $100,000; let's say there's an immediate 20% drawdown so it's now worth $80,000.

You now withdraw $5,000 --> portfolio now stands at $75,000.

In order for the portfolio to recover back to $100,000, it now needs to grow 34%. If it grows 20% (the amount of the drawdown), it will only recover to $90,000.

If you didn't make that withdrawal, the portfolio would have to grow 25% to recover its initial value. So that 5% withdrawal cost you a difference of 9% in portfolio growth - almost double the amount of your withdrawal. The numbers would be more extreme with larger drawdowns, of course.

Anyway just my POV here...the numbers in backtests may still work out in favor of not holding cash, but I think that's entirely dependent on frequency/severity of market corrections. Those long stretches where the stock market kept going up and up make a big difference, and you'd have to bank on that continuing to happen in the future.

Incidentally - totally agree about the need to view any portfolio as a whole entity, instead of focusing on the one asset that's in the doghouse.

Let's hope that the bull market continues long enough to build up your portfolio for an extra safety margin. And then the crash will come just as I'm getting ready to retire, of course

Your posts make me think about strategies too. Like, I have an idea that if my portfolio grows larger than is needed to finance expenses, I can put the extra into 100% stocks and enjoy both the dividends and the long-term (15 year+) growth.

I remember a heated debate between Wellesley and the PP on another forum but I don't think it was Bogleheads. I do remember that somebody named Medium Tex was the main PP protagonist however.

I went all in with Wellessly for a while because the PP seemed a bit too exotic for my tastes at the time but after I read Harry Browne's book I became convinced that the PP was a better strategy for covering all the bases. And if I remember correctly, he was not a fan of corporate bonds at all which I understand is what makes up most, if not all, of Welleslly's bond allocation.

Have not posted for sometime but wanted to comment on Wellesley, HBPP and withdrawal rates. We finally discovered HBPP in 2009 and implemented in early 2011 with a chunk of Wellesley in VP. Currently have about 60% in HBPP with 30% in Wellesley with 10% in misc. old accounts and extra cash. I have been retired for 10 years and GF for 6 years. We do not have a set withdrawal rate for our portfolio but take money out as needed. For example, we withdrew 6-7% in several major travel years and 4-5% when not travelling as much. Our portfolios are now at the same amount as when we started. I know we are losing money to inflation but our reasoning is to spend more now when we are able and not as much when we can't. We also both draw SS in a fair amount. Time will tell how this will all turn out, but for now, if we can keep out portfolio balances stable, we should be okay.

So it looks like Wellesley is currently at 36.5% is stocks, 63.1% in bonds and .4% in cash.

Desert, if you go your proposed 80/20 route, you'd be about 51% in bonds, 29% in stocks and 20% in gold. If I remember your percentages correctly (60/30/10, right?) you'd essentially be ditching 1/6th of your bonds and doubling the gold portion. Has something basic changed in your view regarding gold? Just curious.

Good point about the possible need for simplicity when for some reason you cannot do that yourself anymore.

Setting up and maintaining the PP seems very easy to me, but I know most people around me have have zero experience or interest in maintaining such a portfolio.

A one-fund solution like Wellesley would be ideal, although I think any conservative low-cost and passive fund would be a good PP alternative in such a case.