Happy New Year all,

Year 2021 returns for my leveraged PP is 32.09%.

My leveraged PP is: 40% UPRO, 30% UBT, 30% UGL. Its approximately 2.3x leverage overall. Here's the PortfolioVisualizer link:

https://www.portfoliovisualizer.com/bac ... tion3_1=30

PP Inspired Leveraged Portfolios

Moderator: Global Moderator

Re: PP Inspired Leveraged Portfolios

Leveraging in effect borrows money in order to scale up exposure to a asset. Simply by dropping cash from the PP to scale up stock/gold/LTT exposure to thirds each is a 1.33x PP.vincent_c wrote: ↑Thu Oct 21, 2021 7:57 pmI did see something about leveraging STTs or ITTs with perhaps what they think is a better risk adjusted return compared to LTTs. I've investigated this myself in the past and concluded it carries both different risks and hidden costs and ultimately was not worth it. I may be wrong about it but it does potentially fall in the splitting hairs/tweaking category of optimizations.

Harry expected one of the PP assets to be losing at any one time. He also said something like

i.e. that one of the assets would do very well over a number of years, perhaps rising 200% or more over a decade/whatever whilst the other assets might be relatively dull.Well there's a interesting thing about investments that people rarely notice during a Bull, Bear, whatever market and that is the investments that are winning have a greater impact upon your portfolio than those that are losing. When a investment is in a Bear market it may do down 25, 35 maybe even 40 or maybe even 50% in some rare occasions, but when a investment is in a Bull market it doesn't go up 25, 35 or 40% but goes up 100% or 200% sometimes 300 or 400%, far far more than some other investment is losing, and as a result any combination of them tends to be driven by the investment that is winning and has a bigger impact on the outcome.

As a alternative to fixed weight leverage, consider these PV views

Straight PP 1980 to 2019. Started with $10K, ended with $178K

>1.33x PP. 1980 - 2019 that ended with $342K by dropping cash and swapping out TSM for more volatile (form of leverage) SCV for the stock.

Now for some rotational action ...

1980-1999. Started with $10K, ended with $157K, holding 50/50 SCV/LTT given that in 1980 the Dow/Gold ratio was down at around 1.0 levels i.e. a prediction in 1980 that gold was unlikely to be the 'big winner'.

Continuing that, $157K invested 2000 to 2009 in 50/50 LTT/gold as the Dow/Gold ratio was very high, up at 40 levels, and other stock valuations methods also indicated extremes. That ended 2009 with $447K.

For 2010 to 2019 50/50 In SCV/Gold saw $447K grow to $1019K. Back at the end of 2009 it was quite widely being proclaimed that longer dated treasury bonds had little growth prospects given such low yields.

Collectively that drop cash, drop the asset that looks to have the weakest 10 year prospect to provide a 200%+ gain, resulted in a 1014 / 178 = 5.7 greater gain factor compared to the straight PP over those 40 years, a 4.4% higher annualized reward.

Going forward, continuing that on for 2020 to 2029, and I'd say dropping LTT's would be reasonable. However Dow/Gold was up at around 19 levels at the end of 2019, also suggesting that stocks were somewhat expensive, as also suggested by PE. If in doubt we can always de-leverage back down to holding a standard 4x25 PP, however LTT's do still seem to have little prospect so might be replaced by cash 25/25/50 TSM/gold/cash perhaps

1980 to date and that rotation set compared in total return to that of 100% TSM, over a period that was pretty good/great for stocks. And with the worst of bad years seeing considerably less downside volatility. Leveraging by selecting the asset you opine is least likely to be the provider of a 200%+ type forward ten year reward.

Re: PP Inspired Leveraged Portfolios

I'm seeing 1.73x average leveraged PP, having provided 2x the reward since 1963 ...

Dropping PP cash to invest in the other three assets = 1.33x leverage

Dropping the asset at the start of each decade that has the lowest prospect to provide a 100%, 200% type reward, leaves just two assets, so 2x leveraged PP. But not applied in all decades - some were inconclusive so in those decades held all three (stocks/gold/LTT).

20 year yield, S&P500 PE and Dow/Gold ratio measures used for relative valuation.

1960's held stock/gold (2x leverage), dropped LTT

1970's held all three, stock/gold/LTT (1.33x leverage)

1980's held stock/LTT (2x leverage), dropped gold

1990's held stock/LTT (2x leverage), dropped gold

2000's held LTT/gold (2x leverage), dropped stocks

2010's held all three stock/gold/LTT (1.33x leverage)

2020's holding stock/gold (2x leverage), dropped LTT

(average leverage 1.73x)

Gain 1963 to 2021 inclusive (linest(ln ...slope of real gain exponential trend line) 8.2% versus 4.2% for conventional PP versus 6.2% for 100% TSM.

The worst (nominal) year was 1969, -13%, but that followed two good years of around +25% gains each. Other than that all other years with negative outcomes were less than -5% losses, similar to the conventional PP.

Since 2020, with stock/gold indicated, 12.14% annualized real to end of 2021

PP with a brain - not holding gold in 1980 when Dow/Gold was down at 1.0 levels, or stocks in 2000 when PE was up at 40 levels, or LTT's in 2020 when yields are down at <2% levels.

1963 - 2021 inclusive average exposure : 36% Stock, 27% Gold, 37% LTT

Dropping PP cash to invest in the other three assets = 1.33x leverage

Dropping the asset at the start of each decade that has the lowest prospect to provide a 100%, 200% type reward, leaves just two assets, so 2x leveraged PP. But not applied in all decades - some were inconclusive so in those decades held all three (stocks/gold/LTT).

20 year yield, S&P500 PE and Dow/Gold ratio measures used for relative valuation.

| Year start Values | 20 year T Yields (%) | S&P500 PE | Dow/Gold Ratio |

| 1963 | 4.19 | 21.04 | 18.45 |

| 1964 | 4.21 | 22.75 | 21.64 |

| 1965 | 4.52 | 23.69 | 24.73 |

| 1966 | 4.58 | 19.74 | 27.30 |

| 1967 | 5.56 | 21.75 | 22.19 |

| 1968 | 5.98 | 22.28 | 25.50 |

| 1969 | 6.94 | 17.33 | 22.50 |

| 1970 | 6.45 | 15.87 | 22.73 |

| 1971 | 5.99 | 16.6 | 22.45 |

| 1972 | 6.03 | 18.65 | 20.46 |

| 1973 | 7.38 | 13.49 | 15.77 |

| 1974 | 7.93 | 8.29 | 7.58 |

| 1975 | 8.04 | 10.25 | 3.29 |

| 1976 | 7.17 | 11.6 | 6.08 |

| 1977 | 7.98 | 9.68 | 7.47 |

| 1978 | 8.99 | 9.01 | 5.02 |

| 1979 | 10.16 | 8.75 | 3.59 |

| 1980 | 12.09 | 9.39 | 1.60 |

| 1981 | 14.04 | 7.83 | 1.64 |

| 1982 | 10.62 | 8.47 | 2.19 |

| 1983 | 11.98 | 9.82 | 2.34 |

| 1984 | 11.70 | 9.6 | 3.30 |

| 1985 | 9.50 | 11.69 | 3.92 |

| 1986 | 7.39 | 14.09 | 4.73 |

| 1987 | 8.89 | 13.39 | 4.85 |

| 1988 | 9.07 | 14.7 | 3.99 |

| 1989 | 7.96 | 17.65 | 5.29 |

| 1990 | 8.17 | 15.85 | 6.87 |

| 1991 | 7.06 | 18.44 | 6.74 |

| 1992 | 7.05 | 20.45 | 8.97 |

| 1993 | 6.48 | 21.16 | 9.92 |

| 1994 | 8.02 | 19.91 | 9.61 |

| 1995 | 6.01 | 25.03 | 10.02 |

| 1996 | 6.73 | 27.72 | 13.23 |

| 1997 | 6.02 | 33.03 | 17.45 |

| 1998 | 5.39 | 38.82 | 27.35 |

| 1999 | 6.83 | 44.19 | 31.94 |

| 2000 | 5.59 | 37.27 | 39.53 |

| 2001 | 5.74 | 30.5 | 39.56 |

| 2002 | 4.83 | 23.1 | 36.24 |

| 2003 | 5.10 | 26.64 | 24.34 |

| 2004 | 4.85 | 27.14 | 25.05 |

| 2005 | 4.61 | 26.44 | 24.62 |

| 2006 | 4.91 | 27.28 | 20.89 |

| 2007 | 4.50 | 25.96 | 19.61 |

| 2008 | 3.05 | 15.38 | 15.86 |

| 2009 | 4.58 | 20.32 | 10.15 |

| 2010 | 4.13 | 22.4 | 9.45 |

| 2011 | 2.57 | 20.52 | 8.21 |

| 2012 | 2.54 | 21.24 | 7.76 |

| 2013 | 3.72 | 24.86 | 7.88 |

| 2014 | 2.47 | 26.79 | 13.80 |

| 2015 | 2.67 | 25.97 | 14.86 |

| 2016 | 2.79 | 27.87 | 16.40 |

| 2017 | 2.58 | 32.09 | 17.23 |

| 2018 | 2.87 | 28.29 | 19.14 |

| 2019 | 2.25 | 30.33 | 18.26 |

| 2020 | 1.45 | 33.77 | 18.88 |

| 2021 | 1.94 | 38.68 | 16.30 |

1960's held stock/gold (2x leverage), dropped LTT

1970's held all three, stock/gold/LTT (1.33x leverage)

1980's held stock/LTT (2x leverage), dropped gold

1990's held stock/LTT (2x leverage), dropped gold

2000's held LTT/gold (2x leverage), dropped stocks

2010's held all three stock/gold/LTT (1.33x leverage)

2020's holding stock/gold (2x leverage), dropped LTT

(average leverage 1.73x)

Gain 1963 to 2021 inclusive (linest(ln ...slope of real gain exponential trend line) 8.2% versus 4.2% for conventional PP versus 6.2% for 100% TSM.

The worst (nominal) year was 1969, -13%, but that followed two good years of around +25% gains each. Other than that all other years with negative outcomes were less than -5% losses, similar to the conventional PP.

Since 2020, with stock/gold indicated, 12.14% annualized real to end of 2021

PP with a brain - not holding gold in 1980 when Dow/Gold was down at 1.0 levels, or stocks in 2000 when PE was up at 40 levels, or LTT's in 2020 when yields are down at <2% levels.

- LPP$.png (132.19 KiB) Viewed 36683 times

1963 - 2021 inclusive average exposure : 36% Stock, 27% Gold, 37% LTT

Re: PP Inspired Leveraged Portfolios

This thread has been dormant for a while so I thought I would refresh it.

Need to do the bad with the former good...through 7/31/22 with quarterly rebalance

UST/TQQQ/VGSH 70/20/10 (The bullet)

VGSH/TQQQ/TMF/DGP 44/25/12.5/18.5 (The barbell) - Note the change from UGLD to DGP and the change in weighting of gold etfs and cash.

VGSH 35%, UST 30%, TQQQ 25%, DGP 5%, VIXY 5% (Newbie 1)

BND 70%, TQQQ 25%, VIXY 5% (Newbie 2)

Bullet: -22%/-30.44%

Barbell: -23.25/-30.19

Newbie 1: -19.30/-26.96

Newbie 2: -19.09/-26.72

Not a great year for sure. I was down around 30% at the end of July. The main difference was I hold more TMF and of course that has been pounded this year as well.

Need to do the bad with the former good...through 7/31/22 with quarterly rebalance

UST/TQQQ/VGSH 70/20/10 (The bullet)

VGSH/TQQQ/TMF/DGP 44/25/12.5/18.5 (The barbell) - Note the change from UGLD to DGP and the change in weighting of gold etfs and cash.

VGSH 35%, UST 30%, TQQQ 25%, DGP 5%, VIXY 5% (Newbie 1)

BND 70%, TQQQ 25%, VIXY 5% (Newbie 2)

Bullet: -22%/-30.44%

Barbell: -23.25/-30.19

Newbie 1: -19.30/-26.96

Newbie 2: -19.09/-26.72

Not a great year for sure. I was down around 30% at the end of July. The main difference was I hold more TMF and of course that has been pounded this year as well.

Re: PP Inspired Leveraged Portfolios

My leveraged PP consists of 40% UPRO, 30% UBT, 30% UGL. Rebalanced yearly. So far YTD (as of 7/31/22) it's down -30.92%.

Although that does suck, if you zoom out, the 3-year annualized return is 25.58%. 5-year annualized return is 23.24%. Not too shabby, but it's definitely a roller coaster ride.

Even though gold is the best performing asset of the 3, it's still negative YTD. I am a bit surprised gold isn't performing better considering the high inflation and geopolitical events. Oh well, let's see where we stand at year end.

Although that does suck, if you zoom out, the 3-year annualized return is 25.58%. 5-year annualized return is 23.24%. Not too shabby, but it's definitely a roller coaster ride.

Even though gold is the best performing asset of the 3, it's still negative YTD. I am a bit surprised gold isn't performing better considering the high inflation and geopolitical events. Oh well, let's see where we stand at year end.

Re: PP Inspired Leveraged Portfolios

My current mix is TQQQ & BND 25%, TMF 30% and GLDM 20%.ozzy wrote: ↑Thu Aug 11, 2022 11:51 am My leveraged PP consists of 40% UPRO, 30% UBT, 30% UGL. Rebalanced yearly. So far YTD (as of 7/31/22) it's down -30.92%.

Although that does suck, if you zoom out, the 3-year annualized return is 25.58%. 5-year annualized return is 23.24%. Not too shabby, but it's definitely a roller coaster ride.

Even though gold is the best performing asset of the 3, it's still negative YTD. I am a bit surprised gold isn't performing better considering the high inflation and geopolitical events. Oh well, let's see where we stand at year end.

I'm not surprised about gold because the dollar has been going up. HB talked about this and my research indicates when the USD is doing well gold will not do that great normally. I'm actually not too disappointed in gold, of course I would have liked it to have done better as well. Gold did well in 2020 which is when I would have expected it to have done well (a lot of uncertainty) and the dollar went down that year as well. If the dollar wouldn't have gone up 10% this year (using UUP as a proxy) I think it would have been a good year for gold.

I hold gold because thus far it does a good job of zigging when other stuff zags (low correlation) and generally has a positive nominal return. However, it's the one asset that I lay no claim to understanding why it does what it does even after having read as much as I could about it from what I consider non-biased sources (academics and firms whose business isn't heavily in the metals markets).

Re: PP Inspired Leveraged Portfolios

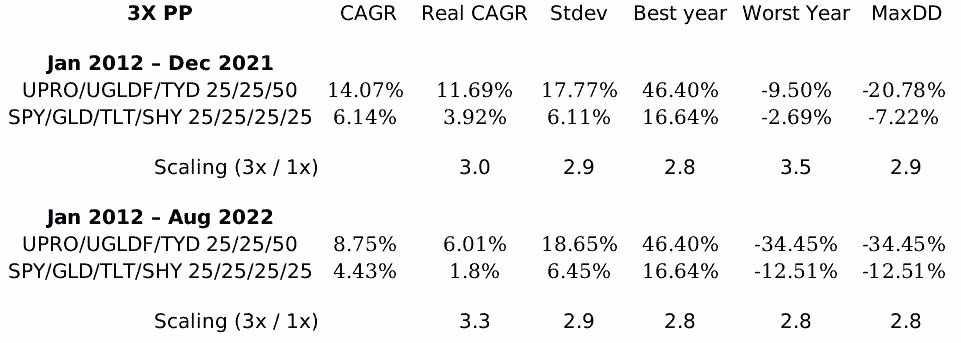

Leveraging is inclined to scale the volatility, not the rewards. Compounded rewards are a factor of yearly average and standard deviation. Scale up both the average AND the standard deviation and that tends to just still yield the same/similar annualized (CAGR)

For leverage to scale CAGR you need multiple assets and inverse/low correlations in order to yield the volatility-pumping (rebalance) benefits, i.e. PP type asset combinations. When so we also see REAL (after inflation) CAGR being scaled

For the decade starting 2012 (to end of 2021) the PP was providing a (near) 4% real, as generally expected. A 3x version (with 50% in 10 year treasury bullet rather than 25% in each of 1 and 20 year barbell) also yielded near 3x that real reward. 3.9% real for the PP, 11.7% real for the 3x.

Add on another 8 months however (to end of August 2022) and the ongoing real CAGR for the PP has dropped to 1.8%, whilst the 3x's has dropped to 6%

With generally all of the PP assets being relatively down recently, the tendency is to subsequently see one (or more) 'pop' to the upside. But the uncertainties that dragged down all assets could see the continuation of that 'all-down' to even deeper levels. However it does feel like we're closer to the bottom of all-four PP assets being down/negative (in real terms) than we are to the average/top, and as such could be a reasonable time to be looking to introduce leverage, such as 50/25/25 TYD/UPRO/UGLDF (3x's), in anticipation of the PP levelling-off/rising.

If/when such a 'pop' occurs that pulls up the PP from 2% real to 4% real, so that might see 3x PP increase from 6% real to 12% real, a potential relatively quick 'double-up' of ongoing real CAGR. PP is down -12.5% for 2022 to end of August and might rebound +15%, whilst 3x PP might +45% over the same period.

I forgot to set the rebalance intervals to quarterly in the above table data, left it (PortfolioVisualizer data) set at the default yearly setting. For 2x you can get away with yearly rebalancing, but with 3x and above you need to rebalance more frequently, at least once each 6 months for 3x. I've left that yearly rebalanced data as in that particular case the figures weren't that different anyway to 6 month or quarterly rebalancing (too lazy to re-download the data, create the table and post a 'corrected' image)

For leverage to scale CAGR you need multiple assets and inverse/low correlations in order to yield the volatility-pumping (rebalance) benefits, i.e. PP type asset combinations. When so we also see REAL (after inflation) CAGR being scaled

For the decade starting 2012 (to end of 2021) the PP was providing a (near) 4% real, as generally expected. A 3x version (with 50% in 10 year treasury bullet rather than 25% in each of 1 and 20 year barbell) also yielded near 3x that real reward. 3.9% real for the PP, 11.7% real for the 3x.

Add on another 8 months however (to end of August 2022) and the ongoing real CAGR for the PP has dropped to 1.8%, whilst the 3x's has dropped to 6%

With generally all of the PP assets being relatively down recently, the tendency is to subsequently see one (or more) 'pop' to the upside. But the uncertainties that dragged down all assets could see the continuation of that 'all-down' to even deeper levels. However it does feel like we're closer to the bottom of all-four PP assets being down/negative (in real terms) than we are to the average/top, and as such could be a reasonable time to be looking to introduce leverage, such as 50/25/25 TYD/UPRO/UGLDF (3x's), in anticipation of the PP levelling-off/rising.

If/when such a 'pop' occurs that pulls up the PP from 2% real to 4% real, so that might see 3x PP increase from 6% real to 12% real, a potential relatively quick 'double-up' of ongoing real CAGR. PP is down -12.5% for 2022 to end of August and might rebound +15%, whilst 3x PP might +45% over the same period.

I forgot to set the rebalance intervals to quarterly in the above table data, left it (PortfolioVisualizer data) set at the default yearly setting. For 2x you can get away with yearly rebalancing, but with 3x and above you need to rebalance more frequently, at least once each 6 months for 3x. I've left that yearly rebalanced data as in that particular case the figures weren't that different anyway to 6 month or quarterly rebalancing (too lazy to re-download the data, create the table and post a 'corrected' image)

Re: PP Inspired Leveraged Portfolios

Thank you for the post! It was great.

If one breaks down the PPs performance profile it’s definitely cyclical/exhibits return to mean behavior. I do think we will see some outperformance whenever this down cycle ends.

If one breaks down the PPs performance profile it’s definitely cyclical/exhibits return to mean behavior. I do think we will see some outperformance whenever this down cycle ends.

Re: PP Inspired Leveraged Portfolios

Thanks.

Europe will have a hard winter (energy prices are a lot higher than in the US), much money has flown into the US (safety), hence gold price in USD has been rather flat despite significantly negative real yields (rising/high inflation). Once winter is over, and Europe has redirected its sources of energy supply/gas prices start to decline and uncertainties decline. I suspect they'll be a outflow out of USD to 'better value' elsewhere, strong USD giving up some of its strength, gold prices rising in USD. As such my guess is that 50/50 3x UPRO/UGLDF to scale up leverage to in effect 6X could prove to be generous (both up). Perhaps a January start time point, in anticipation of a better (European) 2023, at least as things stand as they presently are.

Re: PP Inspired Leveraged Portfolios

Are you the same seajay as on Bogleheads?

Re: PP Inspired Leveraged Portfolios

Considering counter-party risk, bank deposits = banks money, your name recorded in its creditors book; Stock purchases = shares registered in the brokers name, your name recorded in its creditors book. Worsened by governments looking to push the transition away from taxpayers based bailouts towards savers/investors bail-ins. With a "if you can't touch it, you don't own it" philosophy diluting down that counter-party risk, that could present at any time during a 20 or 30 year horizon period, and a reasonable choice might be the Talmud style thirds land (own home), stocks, and physical gold ... that has 33% counter-party risk (stocks). However we might reduce that risk further by replacing the 33% stock with 11% in a 3x stock LETF. Backtesting using assumed cost of borrowing (scaling up exposure) of T-Bill + 2% indicate some reasonable rewards from that mostly 'custodial' (in-hand) style. More black-swan protection ... if stocks/bonds dive holding some gold, or if depository falters with contagion (knock-on) then being largely custodial .. might see you considerably richer than others who hadn't held any gold or were fully loaded into counter-party risks.

Re: PP Inspired Leveraged Portfolios

Happy New Year all,

Year 2023 returns for my leveraged PP is 30.98%. Its clawing its way back from the hellish -41.67% Year 2022 return.

If interest rates have in fact topped, then bond funds (TLT, UBT) may have bottomed.

Here's the PortfolioVisualizer link to my leveraged PP:

https://www.portfoliovisualizer.com/bac ... a1nPbzER16

Year 2023 returns for my leveraged PP is 30.98%. Its clawing its way back from the hellish -41.67% Year 2022 return.

If interest rates have in fact topped, then bond funds (TLT, UBT) may have bottomed.

Here's the PortfolioVisualizer link to my leveraged PP:

https://www.portfoliovisualizer.com/bac ... a1nPbzER16

Re: PP Inspired Leveraged Portfolios

Hey can you break out the gain for each asset in 2024

That's amazing 30 pct

Upro

Ugld

The bond hold must have gotten killed.

That's amazing 30 pct

Upro

Ugld

The bond hold must have gotten killed.