Re: P2P Lending

Posted: Fri Jun 10, 2016 9:53 pm

This is massively inaccurate, so have fun with it:

http://www.nytimes.com/2016/05/15/busin ... tails.html

http://www.nytimes.com/2016/05/15/busin ... tails.html

Permanent Portfolio Forum

https://www.gyroscopicinvesting.com/forum/

https://www.gyroscopicinvesting.com/forum/viewtopic.php?t=3176

I've no problems. I was just on it a few days ago for the statements and just now. Do a traceroute?sophie wrote:I'd look into the stats to see if there really has been a jump but...

It's been 3 days now. Wonder if they use Arvixe.

I think you'll get a kick out of this...sophie wrote:It's been up and down. Down right now but was up briefly last night.

Not so fast! Before you give up, what you need is superior credit intelligence than what LC just provides out of the box. I just logged in to see my stats since Jan 2015:sophie wrote:It looks to me like Lending Club loosened its borrower requirements quite significantly about 2 years ago while reducing interest rates, presumably to attract more borrowers so they can inflate their portfolios and collect more fees. And it works - despite the recent bad press, their loan issuance is still going up. Quite a conflict of interest. It was fun for a while but I think there are better places for VP money.

11 credit cards and 1 personal loan. I really hate to say this (especially in this topic), but just go directly to Chapter 11 (well, in the old days). Do not put your head in the sand like an ostrich and wait it out (in my defense, I was young and naive and interacting with the government was a scary proposition at the time on top of the already very scary situation). However, I wasn't gaming the system like certain P2P borrowers appear to be doing (its really hard to tell with no personal contact with the borrowers, which I also find rather aggravating... not that I want to bust their kneecaps or anything like that!sophie wrote:You went through a charge-off? Sounds like there is a story there worth telling.

Me too, but I think you should giva LA a chance before giving up. It costs you nothing which is a rare opportunity. And they're far superior to LendingRobot which is just run o' the mill and does cost you. There may be others, but I'm not interested. I know a good thing when I see one.sophie wrote:Definitely I'm talking myself out of this investment. I thought Lending Club's self-interest would be enough to protect investors from the worst excesses of the borrowers, but now I'm not so sure of that.

I think I found the reason!sophie wrote:You can expect to recover an average of 10% on charged off loans, after fees.

The greatly increased rate of deadbeat loans continues, and it's mostly loans about 6 months old. I'm curious about the reasons. It may be some fundamental weaknesses in the economy, like the job count glossing over the realities of low paying, part time jobs. I suspect, though, that there just isn't much of an incentive to repay an unsecured loan, and there are probably a lot of people who have figured out that if you're already going to default on a credit card loan, you might as well pick up an extra $35K from a P2P lender on the way. This is outright fraud, but that's hard to prove and near impossible if the person has made 6 payments.

Not sure any unsecured loan scheme is going to be any better. I'm still getting a decent return (~12%) from LC, but it relies entirely on Lending Club somehow limiting the number of fraudulent borrowers, and they have no real incentive to do so.

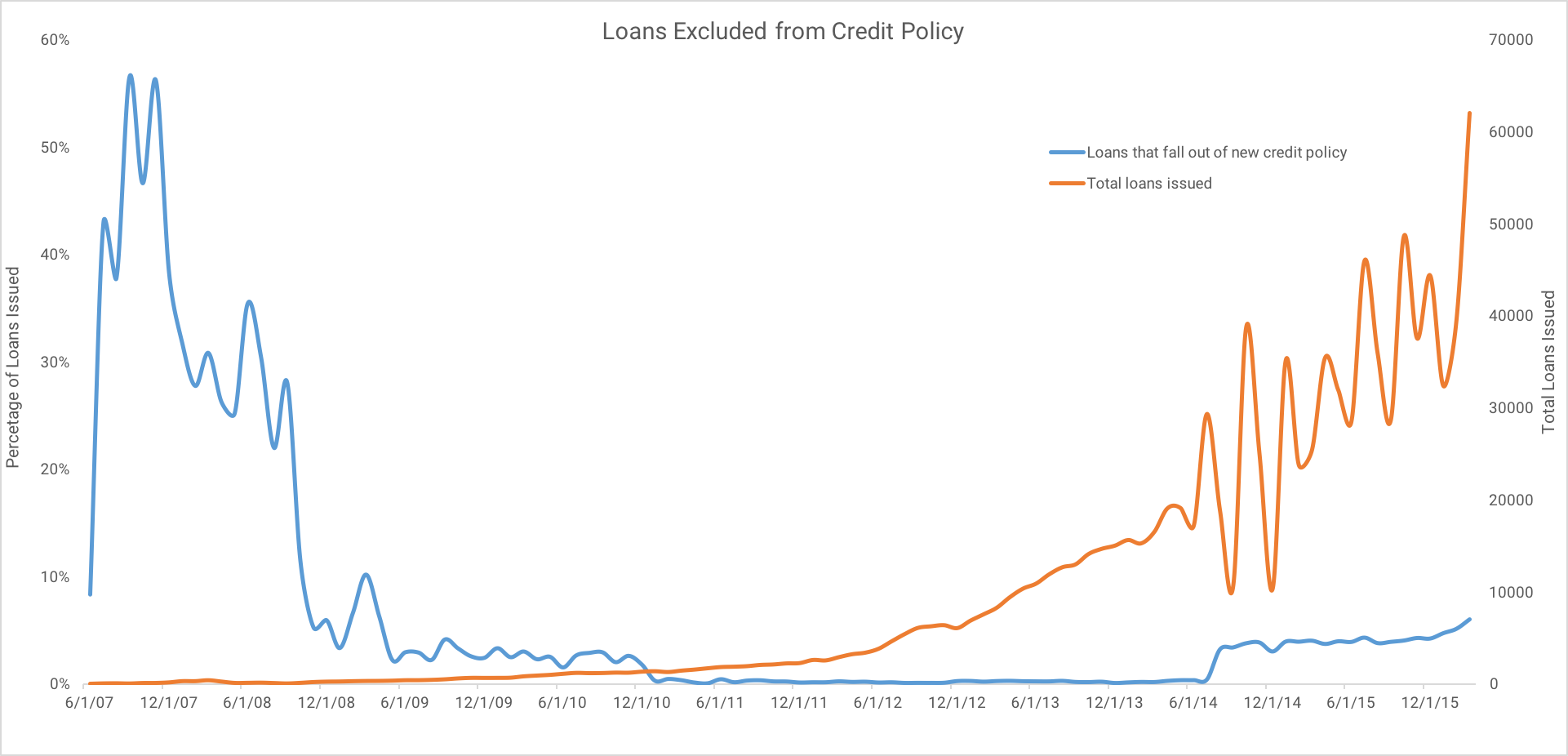

I wonder if this will turn into a race to the bottom as economic malaise trickles up? I really can't emphasize enough that you've got to diversify like you've never diversified before in your life and not just in quantity but over time too. Fortunately, the latest stats from LR show that the 98% confidence level for earning a positive return happens with just 150-200 notes which is nothing. This is not a get rich quick scheme, but 10 years down the line, the yearly cash flow is ginormous! Where else can you actually diversify into positivity other than dividend growth stocks? Very cool.In September 2014 the company loosened its credit policy and raised the acceptable level of a borrower's DTI from 35% to 40%. Borrowers who fell inside this new category represented an immediate increase of 3.2% of originations in August 2014, which has nearly doubled to 6% as of March 2016. Most of these new borrowers fell into grades D-E, which corresponds with higher risk.

In early 2016 Lending Club announced that it had discovered 'pockets of loans that were underperforming expectations'. According to SEC filings, Lending Club tightened credit requirements effective June 7th, 2016, returning DTI limits to 2014 levels. Their reasoning was explained in a 8k filing:

In some higher risk grades in early 2016, we identified some underperforming pockets of loans and made modifications to pricing and credit policies accordingly. The population eliminated from the credit policy represents slightly less than 5% of loan volume (annualized based on Q4 2015), and was mainly characterized by high indebtedness, an increased propensity to accumulate debt and lower credit scores.

Lending Club did not release statistics on how these underperforming segments were affecting investor return. The two questions are therefore,

How poorly were these loans performing?

How will this move affect company revenue?

(Source: Compiled Lending Club data)

Although not directly comparable due to improvements in the company's overall underwriting algorithms, we have some reference to how these borrowers have done as a population as credit was extended to this category from the company's founding until late 2010. All of these notes have now reached maturity, which gives us the opportunity to calculate a definitive ROI. The results are stark: while the platform average return during this period was 7.7%, notes with similar characteristics to the underperforming segment returned -33%.

LendingRobot estimates that the elimination of these poorly performing segments will raise the platform average return by 0.6% to 1%. For those investing in higher-risk borrowers (grades D-G), returns may increase 2% to 3.5%.

http://seekingalpha.com/article/3995758 ... gs-preview

I can't imagine why anyone would do this. It's not like running up debt on credit cards is hard for anyone who is likely to pay it back, so why would they need to borrow from other individuals, unless they are really bad risks?sophie wrote:In case anyone is into Lending Club....

Get out now.

I put a tiny slice of VP money into it as an experiment, just enough to diversify sufficiently. Return's been good (~9%) but in the past several months I've seen a constant stream of loans going bad. The company's claimed charge-off rate is absurdly low. At the current pace, I expect that at least 1/3 - 1/2 of my loans will ultimately charge off. And, the recoveries have shrunk to less than 1% of charged-off amounts, as opposed to the 10% I was getting previously.

Either the economy is not nearly as healthy as advertised, or LC has decided to dump investors overboard and aren't going after deadbeat borrowers. Not good news either way. I guess P2P lending has run its course, but I wonder about all the big pension funds that bought into it.

...Clearly the P2P lending model is still in the "wild west" stage. But I'll be watching closely, and throwing all the Eram Transport Ltd's out there a few bones...and sticking with the HBPP for my serious capital.What Does Eram Transportation Ltd. Do?

We're a trucking company that transports a variety of goods.

Financial Situation

My business is profitable and growing.

What is the loan for?

We intend to buy new equipment to improve a truck.

Why are we safe to lend to?

I'm a hard worker.