I would get 30 year Dutch bonds for the bond part if I was Dutch. They are currently yielding a little over 1% (source https://ca.investing.com/rates-bonds/ne ... ity_to=290) which can easily go lower in a deflationary event; for comparison Swiss rates are currently below 0.3%.

Similarly for cash I would use Dutch short term bills/bonds. Rates are negative -0.6% but that is an insurance against bank failures. Apparently the market thinks this risk is high. Physical gold storage costs more than that.

Here is what harry Browne had to say about non-american investors (from 'why the best laid plans usually go wrong'):

To me all of this is still valid today, except the part about the American stock market offering more alternatives. There are now plenty of European stock investments to choose from.Permanent Portfolio Alterations for Non-Americans

The suggestions in this book are made with American readers in mind. If you live outside the United States, some of the suggestions I've made for the Permanent Portfolio can be changed. Whether you should use U.S. investments or use investments of the country in which you live depends on how stable and useful you consider the investment markets in the country where you live.

If you are an American living abroad and you expect to return to the U.S. to live within the next few years, it isn't necessary to make any changes from the suggestions I've made. If you don't know when or whether you will return to the U.S., consider making the changes.

The purpose of Treasury bills in the portfolio is to provide stable purchasing power through a default-proof investment in the currency you rely on. So, for U.S. Treasury bills, you can substitute the equivalent investment in the country in which you live. That can be bills, notes, or bonds issued by the government and maturing within one year.

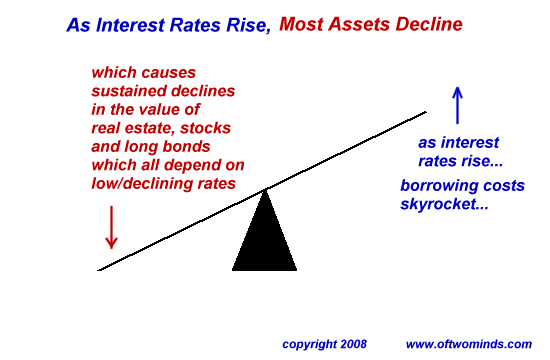

The long-term bonds can be bonds of the government of the country in which you live, so that you will have protection if there's a deflation in your country. Use the longest maturity available.

Stock-market investments are meant to provide profit when your country is prosperous and inflation is low. So, in general, you should

buy stocks of companies in your country.

However, you might prefer to use American stock-market investments instead. Usually, the stock markets of the world move upward or downward together. And the U.S. securities markets offer a greater number of alternatives—including such things as warrants and spe- cialized mutual funds.

The decision may depend upon how adequately you believe you can cover yourself with stock investments of your own country. One pos- sibility is to split the stock-market budget between investments of your country and the United States.

There is no reason to alter the suggestions I've made for gold, no matter where you live.