Page 1 of 9

Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 12:05 pm

by Tyler

I've written before about how the Permanent Portfolio is a really great retirement option, but I always felt like the accumulation side of the equation needed more attention. The common argument that the PP "doesn't earn enough money fast enough" in accumulation always seemed intuitively shortsighted to me, but I couldn't quantify my objection so I let it go. Well, I've done a bit of work and have more insight now. Check out the example here:

Your Ideal Route to Financial Independence May Be Off the Beaten Path

Short story -- yes the PP earns less on average than other stock-heavy portfolios. But thanks to the low volatility, it actually doesn't need to match their returns to beat them to financial independence!

And note that the PP is actually not special in that regard. Typical investing advice is based on quite a myopic view of asset allocation, and when you think beyond traditional stocks and bonds things get really interesting.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 12:20 pm

by mathjak107

then why are the balances in the pp ao much less over most time frames ?

compare balances with funds like wellington , fidelity balanced , even wellesley income and i bet the balances are quite larger so it isn't just about the pp does not fall asw much so ot does need to come back as much .

sure we can cherry pick years the pp did better but i would venture to say more often then not the pp was quite a bit lower balance wise .exclude those 1970 years when you couldn't own gold and the pp didn't exist in concept yet and returns are different .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 12:25 pm

by buddtholomew

Young accumulators are the most vulnerable as they are likely to capitulate and sell at a loss. This early setback could prevent them from investing an entire lifetime. Better in a lower volatility portfolio than a higher one to discover your true risk tolerance. Nice post Tyler.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 12:27 pm

by Tyler

mathjak107 wrote:

then why are the balances in the pp ao much less over most time frames ?

compare balances with funds like wellington , fidelity balanced , even wellesley income and i bet the balances are quite larger so it isn't just about the pp does not fall asw much so ot does need to come back as much .

sure we can cherry pick years the pp did better but i would venture to say more often then not the pp was quite a bit lower balance wise

Read the link! The math behind financial independence is not just about who has the highest balance.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 12:29 pm

by mathjak107

, but when discussing balances and how something does not have to go up as much because it didn't fall as much if you want to compare you need to look at balances . the comparison in that link TO THE PP GOING BACK TO THE 1970'S IS NONSENSE .

no one knows what gold would have done . why not peg the gold to 35 bucks and really let the pp shine in those years we couldn't do it here as well as the concept of it wasn't something introduced to the public .

we all know that allocations are important as far as how the 4% rule holds up but anything in the past over 40% equity's over the worst time frames held up fine . what we don't know is how 25% equity's in the pp would have worked since there was no pp to measure over the worst time frames the 4% safe withdrawal rate is based on which were decades before the pp's existence . .

as far as volatility , that may play a part mentally but mathematically it isn't the amount of the drops that effect the 4% safe withdrawal rate . it is the length of recovery time that is the deciding factor . 2008 saw 40% drops , but recovery was so fast that a retiree in 2008 is no different balance wise then any other retiree in history during average times was the same amount of years in .

even moderate drops if they extend out in time can be fatal to the 4% rule .

when talking about the pp you cannot use the term safe withdrawal rates only withdrawal rates .

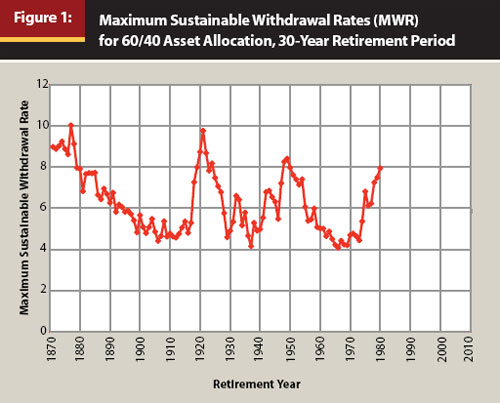

in order to be called safe wiithdrawal rates the portfolio had to specifically stand up to 1907, 1929 , 1937 , 1965/66 . all of which are the absolute worst case scenario's far exceeding the 1970's .

if we rule those out a 60/40 mix would have had a safe withdrawal rate of 6.50% and still have plenty left at the end .

it also isn't about just the income stream not being broken . while the income stream not being broken is one aspect , the balance left at the end of the 30 years is the other and the higher the allocation to stock 90% of the time the bigger balance .

in fact a 60/40 mix at 4% has left more than you started with 90% of the time left over and 2x or more left almost 70% of the time .

that is a huge difference from just the income squeaking through the 30 years .

the article raises all standard retirement issues but mixed them up with terms like safe withdrawal rate and comparisons to the pp in there which can not be compared against the standard the term safe withdrawal rates are based on .

what i don't get is why the constant comparison to other portfolio's trying to spot light the pp by cherry picking data and time frames ?

why not accept it for what it is and does with out trying to feel better about the fact you are doing it by always trying to compare it in some way to more conventional models .

IT IS WHAT IT IS AND IT IS A NICE LOW VOLATILITY PORTFOLIO WITH INSURANCE AGAINST THE COLLAPSE OF THE DOLLAR . JUST LEAVE IT AT THAT INSTEAD OF THIS CONSTANT MENTAL MASTURBATION .

THE FACT IS EVEN 1% DIFFERENCE WOULD MEAN A BALANCE 30 YEARS LATER THAT IS 30% LESS IN BALANCE OR EVEN OR MORE ,SO COMPARISON IS JUST SILLY AGAINST ANYTHING ELSE .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:11 pm

by Tyler

mathjak107 wrote:

, but when discussing balances and how something does not have to go up as much because it didn't fall as much if you want to compare you need to look at balances .

This is incorrect. FI is dictated be the relation between expenses and balances, not by absolute values. Tons of research backs that up.

we all know that allocations are important as far as how the 4% rule holds up but anything in the past over 40% equity's over the worst time frames held up fine . what we don't know is how 25% equity's in the pp would have worked since there was no pp to measure over the worst time frames the 4% safe withdrawal rate is based on which were decades before the pp's existence . .

We've been through this 100 times already, but let me add one new data point. According to Wade Pfau, the single worst year to retire with a traditional 60-40 portfolio since 1926 was in 1966. However, 1973 was REALLY close, with a SWR only 0.2% higher. Retiring in 1973 was on par with

retiring in 1929! So yes there's a difference, but it's smaller than you might think. And importantly, other allocations will have very different high and low years, both in timing and magnitude. When you expand the analysis beyond stocks and bonds, you get interesting results.

as far as volatility , that may play a part mentally but mathematically it isn't the amount of the drops that effect the 4% safe withdrawal rate . it is the length of recovery time that is the deciding factor . 2008 saw 40% drops , but recovery was so fast that a retiree in 2008 is no different balance wise then any other retiree in history during average times was the same amount of years in .

This is mathematically incorrect. Because retirement withdrawals do not care how your portfolio is doing, a deep drop can severely lower your SWR even if the fund recovers the next year. The math is quite clear in that regard. A 4% withdrawal becomes an 8% withdrawal when your portfolio falls 50%. Your portfolio less the withdrawal takes much longer to recover than the pure returns imply. Volatility matters.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:15 pm

by mathjak107

i suggest you read kitces study on the fact that , nooooooo , a sizable drop does not matter as far as sustainability , it is only about recovery time. 2008 was a non event .

as kitces found :

Ultimately, the key point here is simply to recognize that the 2000 retiree is merely ‘in line’ with the 1929 retiree, and doing better than the rest. And the 2008 retiree – even having started with the global financial crisis out of the gate – is already doing far better than any of these historical scenarios! In other words, while the tech crash and especially the global financial crisis were scary, they still haven’t been the kind of scenarios that spell outright doom for the 4% rule.

The viability of a 2008 retiree following the 4% rule is especially notable, and reflects a key (but often ignored or misunderstood) tenet of managing sequence-of-return risk in retirement: it’s actually not just about having a severe market crash in the early years of retirement, but a crash that doesn’t recover quickly. Or more generally, the reality of sequence-of-return risk is that it’s more about having a mediocre decade’s worth of returns, not just a sharp single-year decline that goes through a similarly sharp recovery. And since the markets in the aftermath of 2008 have not stayed down and in fact have been more like a V-shaped recovery (as the S&P 500 has rocketed upwards to now be more than triple its value from the March 2009 trough), it turns out the 2008 financial crisis was an example of something that is not a dangerous sequence-of-returns event after all!

"

https://www.kitces.com/blog/how-has-the ... al-crisis/

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:21 pm

by Tyler

I get it. I just look at many more portfolio options than Kitces does.

mathjak107 wrote:

what i don't get is why the constant comparison to other portfolio's trying to spot light the pp by cherry picking data and time frames ?

why not accept it for what it is and does with out trying to feel better about the fact you are doing it by always trying to compare it in some way to more conventional models .

IT IS WHAT IT IS AND IT IS A NICE LOW VOLATILITY PORTFOLIO WITH INSURANCE AGAINST THE COLLAPSE OF THE DOLLAR . JUST LEAVE IT AT THAT INSTEAD OF THIS CONSTANT MENTAL MASTURBATION .

That's a pretty strong comment coming from a guy dedicated to contrasting his own portfolio to the PP in a PP forum!

I don't cherry pick data. My methods are all on the table and you're welcome to agree with them or not. And not everyone finds challenging the conventional investing wisdom such a waste of time. Rather than spending all day debating details with those who clearly don't care for the analysis, I'll just let the article and data speak for itself and let each person decide whether they find it helpful.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:28 pm

by mathjak107

the pp is fine , i think it is out dated but it is still a low volatile investment ,. the big question is how it will do .

1973 is only considered moderately bad . it is not in the realm of 1965/1966 . 1973 was one of about 4 time frames a new retiree was in the hole year 1 . but it still did better than the 4 standard worst case .

i think the link is fine to play with but i think the pp comparison really does not fit in the context of it , but that is my opinion .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:35 pm

by MachineGhost

Tyler wrote:

And note that the PP is actually not special in that regard. Typical investing advice is based on quite a myopic view of asset allocation, and when you think beyond traditional stocks and bonds things get really interesting.

Thank gawd someone is finally getting it and providing the tools and analysis to do it. You'd likely only see this level of financial analysis in multi-thousand dollar retirement planning software for crony financial advisors, if even at that.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:48 pm

by mathjak107

did you include dividends ? ha ha ha ha

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:49 pm

by mathjak107

i find this article quite interesting . it talks about what made 1965/1966 the bench mark for the worst retirement out come .

http://www.gocurrycracker.com/the-worst ... ment-ever/

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:49 pm

by Tyler

For reference, my numbers are from the Simba spreadsheet via the Bogleheads forum (the same one Craig used for various analyses). Feel free to compare and contrast to your own numbers.

https://www.bogleheads.org/wiki/Simba's ... preadsheet

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:51 pm

by MachineGhost

mathjak107 wrote:

did you include dividends ? ha ha ha ha

Wasn't that. Must been a deranged cell formula as I re-copied and paste. My spreadsheet goes all the way to column BR. Gets very difficult to work with. I get 6.08% CAGR now. Whew!

Back to 1968, the Browne PP is 4.42% and 100% stocks 5.53%.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 1:59 pm

by MachineGhost

mathjak107 wrote:

then why are the balances in the pp ao much less over most time frames ?

Its because the PP is risk overweight gold and the very beginning of its growth in 1972 was a raging gold bull market where everyone thought the dollar was going to collapse. Initial returns matter a great deal 30-years later.

If you compare the PP starting in 1987 and do the same analysis, it looks like it would have been a big loser. Stocks were 7.42% real vs 4.45%. Timing is everything, but style tilting can also add a lot. You really don't realize how lucky you are. But then thats why its best to start significantly investing only after corrections or bear markets. Your future compounded returns will generally be higher. It helps to have a chronically overvalued market for 25 years also (aka P/E expansion).

Wellesly since 1972 was 6.04% real.

Equal Weight Market Cap 7.94% real.

Gold 3.72% real.

Commodities 4.33% real.

Risk Parity PP 4.88% real.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 2:13 pm

by MachineGhost

mathjak107 wrote:

in order to be called safe wiithdrawal rates the portfolio had to specifically stand up to 1907, 1929 , 1937 , 1965/66 . all of which are the absolute worst case scenario's far exceeding the 1970's .

Now this is something you and me finally agree upon. If only there was some way to make silver an effective gold proxy, it would be testable.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 2:39 pm

by mathjak107

there isn't as silver was predominantly an industrial metal with a market so thin that the hunt brothers thought they could manipulate it .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 2:42 pm

by mathjak107

MachineGhost wrote:

mathjak107 wrote:

then why are the balances in the pp ao much less over most time frames ?

Its because the PP is risk overweight gold and the very beginning of its growth in 1972 was a raging gold bull market where everyone thought the dollar was going to collapse. Initial returns matter a great deal 30-years later.

If you compare the PP starting in 1987 and do the same analysis, it looks like it would have been a big loser. Stocks were 7.42% real vs 4.45%. Timing is everything, but style tilting can also add a lot. You really don't realize how lucky you are. But then thats why its best to start significantly investing only after corrections or bear markets. Your future compounded returns will generally be higher. It helps to have a chronically overvalued market for 25 years also (aka P/E expansion).

Wellesly since 1972 was 6.04% real.

Equal Weight Market Cap 7.94% real.

Gold 3.72% real.

Commodities 4.33% real.

Risk Parity PP 4.88% real.

looks right .

but like i pointed out ,even 1% difference is 30% or more at the end of an accumulation stage .

for just a step up in volatility the difference in value between wellesly at 40% equity and the pp was huge. so getting back to the point if you are talking about the pp as an accumulation vehicle i think you could have had far better vehicles . if you want to talk about vehicles for the accumulation stage i wouldn't bring the pp in to the equation unless cherry picking time frames ,.

just leave the pp alone for what it does , it is in a class by itself in that respect and should not be compared .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 2:51 pm

by MachineGhost

mathjak107 wrote:

there isn't as silver was predominantly an industrial metal with a market so thin that the hunt brothers thought they could manipulate it .

If I could ever find semi-numismatic silver coin prices for the era, I think it would be doable. Lots of people hoarded Peace & Morgan silver dollars after the silver standard collapsed.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 3:00 pm

by MachineGhost

[quote=

http://www.gocurrycracker.com/the-worst ... ment-ever/]In what is one of the hardest financial decisions we ever make, we stick to the plan… moving half of our bond position into stock during our annual asset reallocation in ’73, and the other half in ’74. We go all in… 100% stocks. When the world looks to be on the edge of collapse, we fight that clenching feeling in our gut and follow the plan.[/quote]

What was their system or methodology for determining this?

[quote=

http://www.gocurrycracker.com/the-worst ... ment-ever/]

10 Years in daily life is quite enjoyable, but economically things are not looking good. The stock market has crashed, there is no oil, the President Nixon has just resigned, inflation is out of control, and when adjusted for inflation our portfolio is worth only half of what it was when we started[/quote]

Also, I would think there is a minimum amount to be put to gold to survive an environment like this more comfortably. What is it?

So mathjak, have you adjusted your SWR to 3%? Because it said 50/50 @ 4% got destroyed.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 3:24 pm

by craigr

Great post.

I know people that got burned in 2000 and took years to get back into the markets only to get burned again in 2008. They have completely cratered their savings from these experiences. All of these investors would have been much happier in a lower volatility portfolio and would have definitely been further along to their retirement savings program. They got sucked in with promises of high returns but ignored volatility.

Longish quote from our book that discusses this:

Even one year of large losses can be very difficult to recover from (especially for someone who is nearing retirement or already retired).

...

Investors should understand the math involved here because it is not symmetrical. For example, recovering from a 50 percent loss can be very difficult because an investor in that situation will need a 100 percent return just to get back to where he started! Even a 40 percent loss (as happened recently in 2008 to U.S. stocks) requires a 66.7 percent gain to get back to even. Depending on how an investor reacts to these kinds of losses, the recovery could happen in a few years if the investor is patient enough to wait, or it could never happen if the investor bails out due to the stress generated by excessive portfolio volatility.

This problem of large losses hobbling a portfolio potentially for years is why investors want to avoid it. The only way to protect against these kinds of losses is to either take almost no risk (which also means limiting potential gains) or use strong diversification within a portfolio.

...

On one occasion when Craig was working as a network engineer he was discussing network architecture with a very experienced designer, Dr. Jose Nabielsky. Dr. Nabielsky responded to a question about the role of high performance in system design with the following comment: “Speed is fine, just be sure you can take the turns.” The translation is that high performance is only one part of network design; it also has to be reliable at all times to handle inevitable problems.

What does this have to do with investing? A lot. It’s tempting to get enchanted with high performance returns in a portfolio. But, having a portfolio that shows red-hot performance is only one measure you need to consider (and probably not the most important one). Investors also need to know what happens when things don’t go according to plan. Can your investment portfolio take the turns? Or does it go flying off a cliff into a fiery death at the first twist in the road?

Red-hot historical returns are not impressive on their own. It is easy to go into a spreadsheet with historical data and hindsight to come up with a portfolio that outperformed everything else, but that doesn’t mean the portfolio will do that in the future. If investing was that easy there would only be one mutual fund—The Hot Historical Return Fund—and everyone would invest all of their money in it.

Designing a portfolio for high returns alone eventually leads to disaster. Portfolios need the ability to generate growth, but must also have the ability to weather the unexpected storms, including investors’ inevitable bouts of fear when the whole market seems to be falling apart. Portfolios need to take the turns.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 3:33 pm

by mathjak107

50/50 never got destroyed and has a 100% success rate up to 4% . i only need about 3% anyway .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 3:34 pm

by mathjak107

craigr wrote:

Great post.

I know people that got burned in 2000 and took years to get back into the markets only to get burned again in 2008. They have completely cratered their savings from these experiences. All of these investors would have been much happier in a lower volatility portfolio and would have definitely been further along to their retirement savings program. They got sucked in with promises of high returns but ignored volatility.

Longish quote from our book that discusses this:

Even one year of large losses can be very difficult to recover from (especially for someone who is nearing retirement or already retired).

...

Investors should understand the math involved here because it is not symmetrical. For example, recovering from a 50 percent loss can be very difficult because an investor in that situation will need a 100 percent return just to get back to where he started! Even a 40 percent loss (as happened recently in 2008 to U.S. stocks) requires a 66.7 percent gain to get back to even. Depending on how an investor reacts to these kinds of losses, the recovery could happen in a few years if the investor is patient enough to wait, or it could never happen if the investor bails out due to the stress generated by excessive portfolio volatility.

This problem of large losses hobbling a portfolio potentially for years is why investors want to avoid it. The only way to protect against these kinds of losses is to either take almost no risk (which also means limiting potential gains) or use strong diversification within a portfolio.

...

On one occasion when Craig was working as a network engineer he was discussing network architecture with a very experienced designer, Dr. Jose Nabielsky. Dr. Nabielsky responded to a question about the role of high performance in system design with the following comment: “Speed is fine, just be sure you can take the turns.” The translation is that high performance is only one part of network design; it also has to be reliable at all times to handle inevitable problems.

What does this have to do with investing? A lot. It’s tempting to get enchanted with high performance returns in a portfolio. But, having a portfolio that shows red-hot performance is only one measure you need to consider (and probably not the most important one). Investors also need to know what happens when things don’t go according to plan. Can your investment portfolio take the turns? Or does it go flying off a cliff into a fiery death at the first twist in the road?

Red-hot historical returns are not impressive on their own. It is easy to go into a spreadsheet with historical data and hindsight to come up with a portfolio that outperformed everything else, but that doesn’t mean the portfolio will do that in the future. If investing was that easy there would only be one mutual fund—The Hot Historical Return Fund—and everyone would invest all of their money in it.

Designing a portfolio for high returns alone eventually leads to disaster. Portfolios need the ability to generate growth, but must also have the ability to weather the unexpected storms, including investors’ inevitable bouts of fear when the whole market seems to be falling apart. Portfolios need to take the turns.

it had to be bad investor behavior and not markets that did them in . while if you retired in 2000 you are in one of the worst time frames you still are no worse than any other retiree in a similar poorer time frame .

but retire one year later and you are still golden . so picking one year out of 111 rolling time frames as an example really is a poor example .

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 3:36 pm

by craigr

mathjak107 wrote:it had to be bad investor behavior and not markets that did them in .

I don't even think bad investor is the right term. It's more of natural fear of losing everything/loss aversion in humans. Most people will not simply sit back and watch 20, 30, 40% of their life savings evaporate without panicking. They all talk a big game when markets are doing OK, but the first sign of a moderate loss and they are heading for the exit and usually won't return until well after a recovery.

Re: Why the PP is better in accumulation than you think

Posted: Mon Oct 19, 2015 3:38 pm

by mathjak107

no doubt , but then these folks should not be investors . you can't blame markets and these same folks may have long bailed out of the pp too by now .

bad investor behavior will always be with us but you can't blame markets for what happens to them . it didn't happen to many of us , self included ..

interesting enough if you look at morningstar's small investor returns the disparity between what investors got and what the fund got is just as wide on balanced funds as growth funds .

even conservative investing does not seem to help those with no pucker factor

{kind=link}