I hope you are correct!mathjak107 wrote: except as as always , things not even on the radar totally alter what we think is a given when it comes to doom and gloom

Why the PP is better in accumulation than you think

Moderator: Global Moderator

-

Cortopassi

- Executive Member

- Posts: 3338

- Joined: Mon Feb 24, 2014 2:28 pm

- Location: https://www.jwst.nasa.gov/content/webbL ... sWebb.html

Re: Why the PP is better in accumulation than you think

Test of the signature line

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

So do all of us

Re: Why the PP is better in accumulation than you think

Maybe we have to go global and emerging for growth, after some of this current severe decline abates.

Maybe the 21st Century PP is 50% US stocks, 50% non-US, and a big slice of those Emerging markets.20% REIT, 20% Gold, 20% US Treasuries... ooops, that's Meb Faber's Ivy-5 portfolio. The backtesting shows Faber's has almost 3% more CAGR for similar Sharpe ratio. MAXDD is large but isn't terrible at 21.64%.

Maybe the 21st Century PP is 50% US stocks, 50% non-US, and a big slice of those Emerging markets.20% REIT, 20% Gold, 20% US Treasuries... ooops, that's Meb Faber's Ivy-5 portfolio. The backtesting shows Faber's has almost 3% more CAGR for similar Sharpe ratio. MAXDD is large but isn't terrible at 21.64%.

Last edited by ochotona on Sun Nov 01, 2015 9:46 pm, edited 1 time in total.

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: Why the PP is better in accumulation than you think

I don't like unbalanced risk like that. They don't consider that equal weight diversification into a similar asset class is not real diversification. You ultimately need to decide on your top level strategic allocation and then fit everything equally into those three quadrants as the PP does. The Volatility PP Sr is a good start, but the equity exposure is rather low. I think the only guideline we really have is the safe withdrawal rates chart otherwise it seems like a crapshoot to decide what to use for strategic.ochotona wrote: Maybe the 21st Century PP is 50% US stocks, 50% non-US, and a big slice of those Emerging markets.20% REIT, 20% Gold, 20% US Treasuries... ooops, that's Meb Faber's Ivy-5 portfolio. The backtesting shows Faber's has almost 3% more CAGR for similar Sharpe ratio. MAXDD is large but isn't terrible at 21.64%.

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

at some point europe and emerging markets will be where the action is again but still to early . i don't subscribe to that buy low sell high crap . i don't want to fight a trend or try to catch a falling a knife . i want to buy high and sell higher .ochotona wrote: Maybe we have to go global and emerging for growth, after some of this current severe decline abates.

Maybe the 21st Century PP is 50% US stocks, 50% non-US, and a big slice of those Emerging markets.20% REIT, 20% Gold, 20% US Treasuries... ooops, that's Meb Faber's Ivy-5 portfolio. The backtesting shows Faber's has almost 3% more CAGR for similar Sharpe ratio. MAXDD is large but isn't terrible at 21.64%.

which is why my plan has always been dynamic just nudging things slightly towards the longer term trends with the best possibility of playing out , but even if wrong the effect of being wrong is tiny .

just picking up an extra 1% over 30 years is a big difference in performance and balance .

Last edited by mathjak107 on Mon Nov 02, 2015 3:50 am, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

MachineGhost wrote:I don't like unbalanced risk like that. They don't consider that equal weight diversification into a similar asset class is not real diversification. You ultimately need to decide on your top level strategic allocation and then fit everything equally into those three quadrants as the PP does. The Volatility PP Sr is a good start, but the equity exposure is rather low. I think the only guideline we really have is the safe withdrawal rates chart otherwise it seems like a crapshoot to decide what to use for strategic.ochotona wrote: Maybe the 21st Century PP is 50% US stocks, 50% non-US, and a big slice of those Emerging markets.20% REIT, 20% Gold, 20% US Treasuries... ooops, that's Meb Faber's Ivy-5 portfolio. The backtesting shows Faber's has almost 3% more CAGR for similar Sharpe ratio. MAXDD is large but isn't terrible at 21.64%.

the chert is a guideline but the ultimate guideline will still be monitoring your own results for that proverbial 2% real return the first 15 years of retirement .

don't forget how the 1960's had the worst possible sequences the first 15 years and the best market run up in history the next 15 but it was to little to late . they already over spent down their assets the first 15 years .

with results from all asset classes pointing to below average performance this is really going to make things tough to go by what was in the past .

it figures i would retire smack in to it . but luckily our plan has a lot of discretionary spending in it so cutting withdrawals a bit may not be much fun but it can be done .

the good news is the safe withdrawal rates are called safe because they are already so conservative just because they are based around the worst conditions we have had and they were already pretty nasty .

the other good thing is that we will be not only dynamic with the portfolio but dynamic with the budget as each year will be based not on some fixed percentage of an opening balance but on the actual balance yearly .

the issue i have with the "4% rule " is 90% of the time you died with more than you started . not enjoying more things in life that cost money that you could have is not a good thing either .

so even if you go the standard 4% withdrawals inflation adjusted you still need a means of increasing withdrawals or risk leaving to much unspent on the table .

to conservative is no good either ,.

bob clyatt's dynamic spending method automatically gives you more when markets are up .

it can be hard as heck trying to come up with a spending plan using the 4% rule as any increases in a good market can't easily be spent since you are going to need them as a cushion in a down market since the income stream has to remain constant .

the dynamic method does not have a constant income stream . it can vary on the upside unlimited and is limited to just 5% cuts each year on the down side .

but spending methods in retirement are a whole other topic and could be their own discussion and this topic is about the pp in the accumulation stage not the decumulation stage ..

Last edited by mathjak107 on Mon Nov 02, 2015 3:54 am, edited 1 time in total.

Re: Why the PP is better in accumulation than you think

And what might cause that shift? Japan has certainly been trying to get the juices flowing to no avail. And if there is a reasonable chance of high inflation happening in the next few years, then it certainly make sense to hedge against it, right?MachineGhost wrote: I don't see any realistic alternative but to think outside the box.

Either we go the way of the high inflation 1970's and a dollar crisis all over again where real assets shine, including the gold heavy PP.

Or we we go the way of Japan where everything sucks, including the PP, but it eeks out a meager miserable existence. I think the latter is more likely due to the operational reality of the world we live in. At least for a while. Eventually we'll shift to the former.

Yeah, that seems to be the crux of the angst in this thread at the moment. We are hedging for everything but don't see the potential for assets to really shine... only to not stink too badly if conditions are right.MachineGhost wrote: The bigger question is, where will substantial portfolio growth come from? I need growth and I'm having trouble seeing it coming from anywhere but startup investing, real estate and P2P lending. And that may be less true growth than a bubble, but I can't afford to be picky.

If the PP had a downside risk more in line with its meager expected returns, it would be academic in worrying about it...

In an effort to bring this topic back to where Tyler started, yes, I believe that the PP has been a fine growth portfolio up until now. What we are questioning is what will power it going forward?

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

japan blew it day one and there central bank continued to do the wrong thing 2 or 3x . plus japan had very little inflation . they needed very little in gains to sustain life , as well as they did not just have to invest in the Japanese markets .

we are not a japan by any long shot .

we are not a japan by any long shot .

Last edited by mathjak107 on Mon Nov 02, 2015 7:45 am, edited 1 time in total.

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: Why the PP is better in accumulation than you think

The former seems like it will occur when all the foreign sovereign USD-denominated debt at near zero interest rates starts blowing up once the Fed raises. It will be like dominoes collapsing around the world and then eventually it will hit the last man standing, the US. So depending on how slow/clueless/idiotic the ruling/bureaucratic class is at the Fed, NGOs, etc. the SHTF may last a couple of years or it may be nipped in the bud rather quickly as the USD is replaced as the world's reserve currency. Foreign nations will be demanding its replacement because their stupidity would have been no different than the pegging of their currencies to gold in the 1930's. Pegs ALWAYS fail, everywhere and anywhere without exception. If we're very lucky, the US come out of this standing alive. A lot could depend on whether or not we shift to the right politically because you know progressive liberals like Sanders or Clinton would throw us under the bus to sing Kumbaya! with the incestuous NGOs. Those are the same NGO's "advising" the current EU clusterfuck. Not holding my breath here.barrett wrote: And what might cause that shift? Japan has certainly been trying to get the juices flowing to no avail. And if there is a reasonable chance of high inflation happening in the next few years, then it certainly make sense to hedge against it, right?

OTOH, I think Japanization will occur if voters are again stupid and elect more Nanny-State NeoConners, like Sanders, Clinton, Rubio, etc. Pretty much all of the top tier lot except for Trump, Fiorina, Kasich and Christie. We need a wholesale shakeup of overregulation, not more of the same Bullshit That Has Gone Before. Stagnation and loss of confidence is what causes persistent deflation. Japan has a lack of immigration, women are second class citizens, a ridiculously huge and aged population and they don't date, bother to have sex or get married. It's a whole litany of social issues that we really don't have yet, so economic overregulation is the immediate #1 risk, i.e. turning more and more into that socialist basketcase called France.

Its also quite possible we can have both scenarios occuring one after another or even at the same time!

I think we have a few years left while the Middle Eats does their stupid religious war. There's not enough retail participation in the equity market for another bubble top yet, but I think legal startup investing will light a fire under their ass.

Hey, that's just my opinion, but I could be wrong!

Last edited by MachineGhost on Mon Nov 02, 2015 11:28 am, edited 1 time in total.

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

-

Kriegsspiel

- Executive Member

- Posts: 4052

- Joined: Sun Sep 16, 2012 5:28 pm

Re: Why the PP is better in accumulation than you think

You may be right about all this. Except for the sex part. The Japanese DO have sex, it's just with tentacle monsters.MachineGhost wrote:The former seems like it will occur when all the foreign sovereign USD-denominated debt at near zero interest rates starts blowing up once the Fed raises. It will be like dominoes collapsing around the world and then eventually it will hit the last man standing, the US. So depending on how slow/clueless/idiotic the ruling/bureaucratic class is at the Fed, NGOs, etc. the SHTF may last a couple of years or it may be nipped in the bud rather quickly as the USD is replaced as the world's reserve currency. Foreign nations will be demanding its replacement because their stupidity would have been no different than the pegging of their currencies to gold in the 1930's. Pegs ALWAYS fail, everywhere and anywhere without exception. If we're very lucky, the US come out of this standing alive. A lot could depend on whether or not we shift to the right politically because you know progressive liberals like Sanders or Clinton would throw us under the bus to sing Kumbaya! with the incestuous NGOs. Those are the same NGO's "advising" the current EU clusterfuck. Not holding my breath here.barrett wrote: And what might cause that shift? Japan has certainly been trying to get the juices flowing to no avail. And if there is a reasonable chance of high inflation happening in the next few years, then it certainly make sense to hedge against it, right?

OTOH, I think Japanization will occur if voters are again stupid and elect more Nanny-State NeoConners, like Sanders, Clinton, Rubio, etc. Pretty much all of the top tier lot except for Trump, Fiorina, Kasich and Christie. We need a wholesale shakeup of overregulation, not more of the same Bullshit That Has Gone Before. Stagnation and loss of confidence is what causes persistent deflation. Japan has a lack of immigration, women are second class citizens, a ridiculously huge and aged population and they don't date, bother to have sex or get married. It's a whole litany of social issues that we really don't have yet, so economic overregulation is the immediate #1 risk, i.e. turning more and more into that socialist basketcase called France.

Its also quite possible we can have both scenarios occuring one after another or even at the same time!

I think we have a few years left while the Middle Eats does their stupid religious war. There's not enough retail participation in the equity market for another bubble top yet, but I think legal startup investing will light a fire under their ass.

Hey, that's just my opinion, but I could be wrong!

You there, Ephialtes. May you live forever.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

i have a yen for a japanese call girl ha ha ha

Re: Why the PP is better in accumulation than you think

I am retiring in two years. I have the classic 25% PP. If I retired two years ago and drew out 4%, I am guessing I would down close to 8% since PP earned next to nothing in this time period. Assuming this is the case, what would I have to drop down to the the third year to avoid depleting my portfolio to the point that it would not come back to par as far as not outliving the money, assuming another 25 years of life? The original PP had money rates earning something in the 5% range. The money portion is now dead in the water with almost negative rates. Stocks and bonds keep the combination from outperforming enough to over come the shortfall in the cash portion. Gold is a wild card mainly for protection which can go many years before rebounding and can drop even futher due to its extreme volatility. What's everyone's take on this?

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

i use a dynamic method of spending in retirement .

4% of each years balance each dec 31st .

if markets are down i take 5% less then the previous draw or the same draw , which ever is higher .

if the 2nd year is down then it is the same story , 4% of the balance or 5% less , which ever is higher .

because it is dynamic it back tested out 1005 past 40 years of spending

4% of each years balance each dec 31st .

if markets are down i take 5% less then the previous draw or the same draw , which ever is higher .

if the 2nd year is down then it is the same story , 4% of the balance or 5% less , which ever is higher .

because it is dynamic it back tested out 1005 past 40 years of spending

Re: Why the PP is better in accumulation than you think

You say you draw out 4% a year. Call me dumb but could you clarify how this works to keep you from depleting your core balance? You say if "the markets are down, you take less then 5% less of the previous draw." How much less? You are taking out on 4% so you would have a negative draw? Is that right? Can you explain this again in another way as I don't really have my head wrapped around it? example, you take 4% a year Dec 31st. The markets are down (how far down, the market or my PP?). In this case you take 5% less then the year before where the year before you took 4%, huh? I am missing something here.

Last edited by portart on Tue Nov 03, 2015 10:36 am, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

okay , day 1 of retirement you have 1 million clams saved .

you can start with a 40k paycheck first year .

next dec 31st you have an up year and have 1,200.000 .00 so your pay check is now 48k .

3rd year we have a bad year and you are back to 1 million on dec 31 .so you are going to take which ever is higher 4% of the million which is 40k or 48k less the 5% which is 45,600.00 . in this case 45,600 is higher and that is your new pay check for the year .

4th year you repeat and take nother 5% pay cut if need be .

the idea is this keeps you from having to take huge pay cuts if say we fall 40% . for your portfolio to survive only small cuts are needed with this method of withdrawals .

you can start with a 40k paycheck first year .

next dec 31st you have an up year and have 1,200.000 .00 so your pay check is now 48k .

3rd year we have a bad year and you are back to 1 million on dec 31 .so you are going to take which ever is higher 4% of the million which is 40k or 48k less the 5% which is 45,600.00 . in this case 45,600 is higher and that is your new pay check for the year .

4th year you repeat and take nother 5% pay cut if need be .

the idea is this keeps you from having to take huge pay cuts if say we fall 40% . for your portfolio to survive only small cuts are needed with this method of withdrawals .

Last edited by mathjak107 on Tue Nov 03, 2015 12:13 pm, edited 1 time in total.

Re: Why the PP is better in accumulation than you think

Let's say you literally retired two years ago, on November 2, 2013. From peaktotrough.com, with a portfolio of $1 million (and dividends reinvested), we get the following numbers:portart wrote: I am retiring in two years. I have the classic 25% PP. If I retired two years ago and drew out 4%, I am guessing I would down close to 8% since PP earned next to nothing in this time period. Assuming this is the case, what would I have to drop down to the the third year to avoid depleting my portfolio to the point that it would not come back to par as far as not outliving the money, assuming another 25 years of life? The original PP had money rates earning something in the 5% range. The money portion is now dead in the water with almost negative rates. Stocks and bonds keep the combination from outperforming enough to over come the shortfall in the cash portion. Gold is a wild card mainly for protection which can go many years before rebounding and can drop even futher due to its extreme volatility. What's everyone's take on this?

Initial values of stocks, bonds, cash, gold, and total PP:

11/2/2013: 250,000 250,000 250,000 250,000 1,000,000

After one year:

11/2/2014: 290,416 289,363 250,325 223,177 1,053,281

That's a gain of 5.3%. Withdrawing 4% from cash, that's $42,131, gives the following allocation:

11/2/2014: 290,416 289,363 208,194 223,177 1,011,150

The next year elapses:

11/2/2015: 307,067 303,056 208,714 215,414 1,034,251

That's a gain of 2.3%. Withdrawing 4% ($41,370) from cash gives:

11/2/2015: 307,067 303,056 167,344 215,414 992,881

Overall, you would be down less than 1% from your starting million. Would this return be worse from a different starting date? Perhaps. But we can see from this example that the PP hasn't been performing too badly recently.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

your master score card is this :

you need to maintain at least a 2% real return average for the first 15 years of a 30 year retirement to stand up to the traditional 4% safe withdrawal rate .

if you are getting less than that 7 years or so in you need to cut back the pay check .

if you fail to get that 2% real return for the first 15 years then there will not be enough left to grow even if markets do turn around after that .

you need to maintain at least a 2% real return average for the first 15 years of a 30 year retirement to stand up to the traditional 4% safe withdrawal rate .

if you are getting less than that 7 years or so in you need to cut back the pay check .

if you fail to get that 2% real return for the first 15 years then there will not be enough left to grow even if markets do turn around after that .

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: Why the PP is better in accumulation than you think

How much slack is there? Can you miss a couple or a string of years and make it up later before the 15th year, or MUST each and every year be at least 2% real return without exception?mathjak107 wrote: if you fail to get that 2% real return for the first 15 years then there will not be enough left to grow even if markets do turn around after that .

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

yes , in fact that is what will happen as sequence risk takes over . however being down for an extended period of time day 1 before an up cycle develops that cushion could seriously effect your outcome . the first 5 years can be pretty crucial to the success of the retirement while the first 15 determine the entire 30 year plus outcome .

follow that ?

this why methods like the rising glide path are now becoming popular to protect the early years when the most damage can be done .

follow that ?

this why methods like the rising glide path are now becoming popular to protect the early years when the most damage can be done .

Last edited by mathjak107 on Tue Nov 03, 2015 1:26 pm, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

keep in mind it isn't the size of the drop at all that hurts a retirement which is why draw down is a mental thing more than mathamatical . it is the length of time a recovery takes that is key .

even a modest drop for a couple of years can do damage which is why even the pp can be at risk as a retirement portfolio , for a 2008 retiree it was a non event financially , perhaps not mentally because the recovery was so quick .

those who retired in 2008 are on track to be no different then any other retiree in any other normal time frame .

the y2k retiree is very different and they are on track to match the 1929 retiree which means income wise they will get through most likely but with very little left .

90% of the time retirees with a 50/50 mix or 60/40 following the 4% swr have ended with more than they started so the y2k retiree is on track to rival the 1929 retiree .

even a modest drop for a couple of years can do damage which is why even the pp can be at risk as a retirement portfolio , for a 2008 retiree it was a non event financially , perhaps not mentally because the recovery was so quick .

those who retired in 2008 are on track to be no different then any other retiree in any other normal time frame .

the y2k retiree is very different and they are on track to match the 1929 retiree which means income wise they will get through most likely but with very little left .

90% of the time retirees with a 50/50 mix or 60/40 following the 4% swr have ended with more than they started so the y2k retiree is on track to rival the 1929 retiree .

Last edited by mathjak107 on Tue Nov 03, 2015 1:45 pm, edited 1 time in total.

Re: Why the PP is better in accumulation than you think

Both the size and duration of the drop matter. Unless you intentionally cut back your expenses in the down year (a fine idea, BTW), your fixed expenses (that do not shrink with your portfolio decline) will take out a large chunk of your investments and greatly prolong the recovery time to get back to where you were before. Drawdown complicates the recovery time, and volatility does have a measurable effect on withdrawal rates.mathjak107 wrote: keep in mind it isn't the size of the drop at all that hurts a retirement which is why draw down is a mental thing more than mathamatical . it is the length of time a recovery takes that is key .

even a modest drop for a couple of years can do damage which is why even the pp can be at risk as a retirement portfolio , 2008 was a non event because the recovery was so quick .

You're correct about the performance percentages of a 60/40 portfolio, and it's a fine choice in retirement. But using the same methodology other portfolios (including the PP) have supported higher withdrawal rates 100% of the time over the data we have available. One is free to choose the portfolio with the longer data set if that makes them feel more comfortable, but ignoring good opportunities simply because Ibbotson Associates didn't include those assets in their annual returns yearbook that the Trinity and Bengen studies used is up to the individual.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

not quite true about steep drops , michael kitces did a paper on this . it is only the duration . a steep drop like 2008 was a non event to its success rate .. a modest drop over an extended duration has far more serious consequences .

the worst case scenario's the 4% safe withdrawal rate is based on already expects steep drops . that is why it is called a safe withdrawal rate . all it cares about is the 15 year average is at least a 2% real return .

https://www.kitces.com/blog/how-has-the ... al-crisis/

the worst case scenario's the 4% safe withdrawal rate is based on already expects steep drops . that is why it is called a safe withdrawal rate . all it cares about is the 15 year average is at least a 2% real return .

https://www.kitces.com/blog/how-has-the ... al-crisis/

Last edited by mathjak107 on Tue Nov 03, 2015 2:04 pm, edited 1 time in total.

-

dutchtraffic

- Executive Member

- Posts: 242

- Joined: Sat Apr 11, 2015 7:28 am

Re: Why the PP is better in accumulation than you think

You keep assuming things always recover within a year or so, clearly this is nonsense.

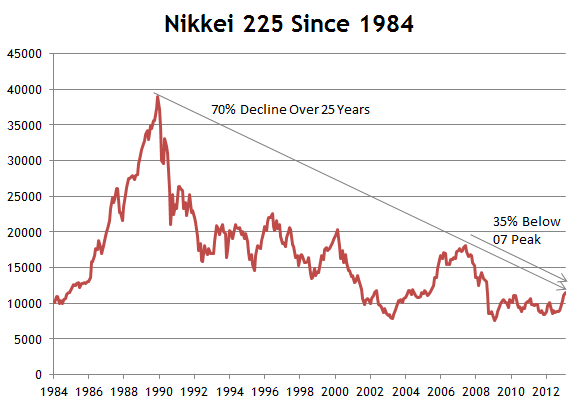

Now what..? US is replaying this scenario now.

Now what..? US is replaying this scenario now.

Re: Why the PP is better in accumulation than you think

From the Kitces paper (empahsis added):mathjak107 wrote: not quite true about steep drops , michael kitces did a paper on this . it is only the duration . a steep drop like 2008 was a non event to its success rate .. a modest drop over an extended duration has far more serious consequences .

He doesn't say the severity of the drop does not matter. Only that the recovery time also matters. I don't disagree with that at all. Also note that he's discussing the survival of a stock/bond portfolio (that I do not dispute), while I'm comparing performance of two different portfolios. Other portfolios he does not consider also do quite well while avoiding both the sharp and long declines.The viability of a 2008 retiree following the 4% rule is especially notable, and reflects a key (but often ignored or misunderstood) tenet of managing sequence-of-return risk in retirement: it’s actually not just about having a severe market crash in the early years of retirement, but a crash that doesn’t recover quickly.

Last edited by Tyler on Tue Nov 03, 2015 2:10 pm, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4662

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

on the other hand the y2k retiree is the one in possible trouble .