I am not convinced HB would change his views based on today's environment, I've been re-listening to the HB radio shows which is his most recent thinking I think he would stick to 4x25 and say its all the same speculation he's heard for 5 decades claiming one asset had reached its end and to move into another. People said the same things "Can rates go lower?" "Rates are only up from here" "What about inflation?" "Is the LTT bull run is over?". The mere asking of these questions means you're speculating and predicting the future. You don't buy the bonds based on yield or what is happening in the economy, you buy the longest bonds you can no matter what because that is the best deflation protection you can buy at the time. He's also said if you're philosophically opposed to government bonds, buy the longest corporate bonds with the highest credit ratings, doesn't need to be treasuries.Kevin K. wrote: ↑Sun Sep 13, 2020 10:37 amThis is a really great post! And I really appreciate the points you and mathjak107 are driving home here - including that with no disrespect for Harry Browne's genius both he and his recommendations were products of their time - how could it be otherwise?ahhrunforthehills wrote: ↑Sat Sep 12, 2020 10:33 pmI think that using TIME as a factor oversimplifies these dynamics. TIME is not what realigns correlations, it is the underlying factors.

This situation is the equivalent of building a teeter-totter on a hill. The lower rates get, many more external factors start coming into play which impact correlations (or lack thereof).

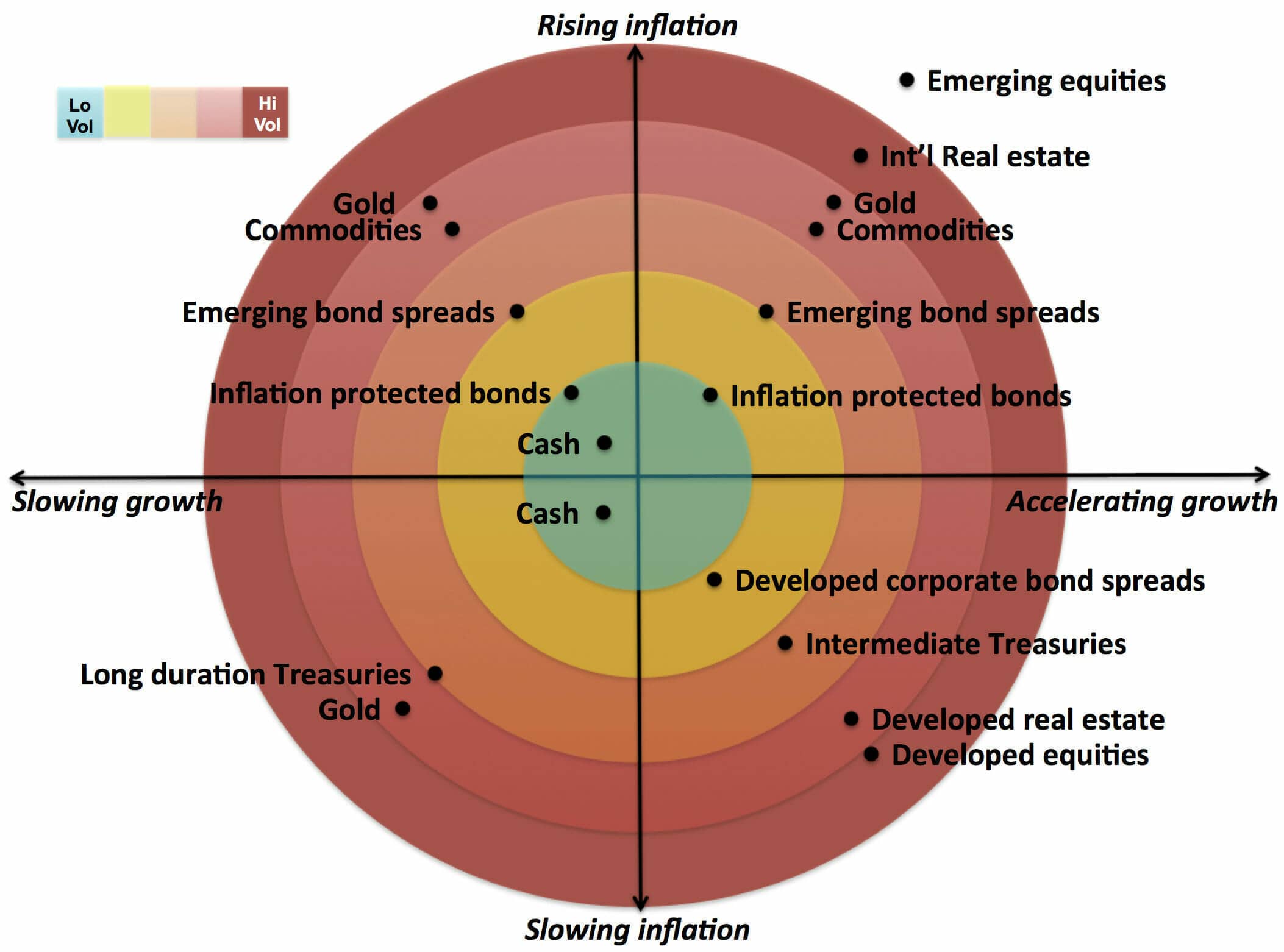

Fun fact, in case you were unaware, in 1981 Browne was advising people to adjust their holdings based on expected inflation levels. He had 6 different options of varying levels of deflation/inflation. Long story short, he would have advised 5% LTT if you were “Uncertain” about inflation levels going forward. It looks like he advised an LTT allocation of -10% (yes, that is a NEGATIVE) if you expected “Rising Inflation” (and by -15% if you were expecting “Runaway Inflation”).

1981 was of course the very end of a 30+ year LTT rate increase from 2.09% to 14.14% that began around 1946.

After he wrote those words, yields went from 14.14% in 1981 to 0.74% in 2020. Not a surprise at all that he later up’d his LTT allocation to 25% in the middle of that falling rate environment.

Harry Brown seemed to suffer from the same recency bias as every other human. He literally came up with the PP in the midrange of those interest rates coming down.

If I split the difference between Harry Brown #1 (recency bias of rising rates) and Harry Browne #2 (recency bias of falling rates) I still come up with about 10% LTT holdings (if not less)

Harry Browne today would have dumped the 4x25 PP in a heartbeat as LTT interest rates approach zero. No doubt.

What I've come around to - and I'm nowhere near as well-versed in the entire body of Browne's work (radio shows, interviews, etc.) as you folks are - is the view that the principles Browne taught (diversification of assets based on economic conditions, not just backtesting, a healthy distrust of both Wall Street and Washington, etc.) are "Permanent" but the 4 x 25% isn't.

The PP is based on the economic conditions from Austrian economics (the business cycle). Inflation, Deflation, Prosperity, Recession. If you don't agree with Austrian economics then the PP won't agree with you haha. However substituting a deflation asset like LTTs for another deflation asset such as STTs or even cash I think HB would agree it wouldn't break the PP but he would say you would lose the "kick" the long bonds give you during deflation.

Whether you stick with LTTs or move to cash it doesn't really matter, you're going to do better than the average investor out there.

{kind=link}